The Amsterdam-Rotterdam-Antwerp (ARA) region, long established as a premium hub for gasoline blending, finds itself at a crossroads. The confluence of regulatory changes and market dynamics is reshaping the landscape, compelling a strategic reassessment of ARA’s role in this sector.

Regulation and market shifts are increasing pressure on ARA gasoline terminals.

The introduction of stringent regulations by the Dutch ‘Inspectie Leefomgeving en Transport’ (ILT) in 2022, aimed at curtailing the export of low-quality gasoline with high sulphur and benzene content, has set off a chain of events. While the ILT’s measures were designed to prevent the Netherlands from being a conduit for ‘dirty’ gasoline, particularly to West Africa, the outcome has been less straightforward.

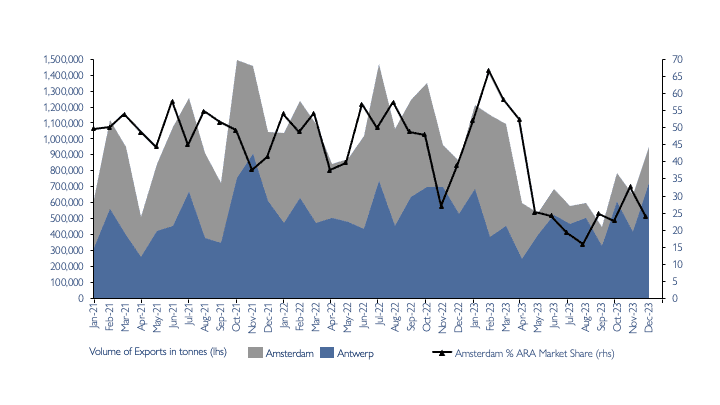

Contrary to the ILT’s expectations, the consequence has been a geographical shift in blending activities, with Antwerp emerging as a beneficiary, maintaining its export volumes to West Africa. The decline in West African demand for ARA’s gasoline is more attributable to Nigeria’s subsidy removal than to regulatory changes in the Netherlands.

GASOLINE EXPORTS TO WEST AFRICA FROM AMSTERDAM AND ANTWERP 2021-2023

Source: Vortexa

Belgium now faces a dilemma: whether to emulate the Dutch model and risk a similar diversion of trade routes. The experience of Amsterdam suggests that such regulatory alignment might merely reroute the supply of lower-quality gasoline to other regions, rather than eliminate it.

Complicating matters further, Russia and the Middle East are stepping up their gasoline exports to West Africa, exploiting price discounts and blending opportunities. This development, coupled with emerging blending hubs in Tunisia and Estonia, signals a potential decentralisation of the market.

Economic Implications for ARA

For ARA terminals, these shifts portend a significant impact. The relocation of blending activities will erode revenues. Traders value the efficiency of proximity in blending operations. Optimising between Amsterdam and Antwerp is harder than in a single port or terminal, but still reasonably efficient. However, if a proportion of the blending activity is no longer permitted a wider relocation of activity will occur. While some high-sulphur components might still pass through ARA, many streams both high and low sulphur will move elsewhere.

The start of the Dangote refinery adds further challenges.

Adding to the complexity is the impending launch of the Dangote refinery in Nigeria.

The volumes of gasoline produced are huge and intended to make Nigeria self-sufficient but that does not mean that all production will stay in Nigeria. The refinery is designed to make European gasoline grades, but without local regulation changes and resulting price rises, the domestic market may not receive the refinery-produced tonnes.

The drive to maximise revenue, combined with the logistical benefit of large ship export capability, may incentivise Dangote to export, even while the high sulphur continues to flow into the country.

Dangote exports would compete in some of the markets currently supplied by ARA, making life more difficult for blenders there. The suppliers of high-sulphur gasoline into West Africa may be in a prime position to manage the Dangote exports and choose to take them to the new blend hubs rather than to ARA.

Strategic Imperatives for ARA

In this evolving landscape, ARA terminals face a stark dichotomy. Those equipped with state-of-the-art facilities and oriented towards transatlantic exports may maintain, or even enhance, their market share. However, terminals that are less well-equipped or logistically constrained could find themselves increasingly marginalised.

This situation is further exacerbated for terminals operating under ILT-style regulations, as they risk losing market share to locations with more lenient regulatory frameworks, provided these alternatives offer competitive blending services.

The Urgency of Adaptation

The need for a strategic overhaul is palpable. ARA terminals must urgently contemplate repurposing strategies, which could include accelerating the energy transition, exploring new products or markets, or even considering investments in processing capabilities. This pivot is not merely a matter of staying relevant but is essential for survival in a rapidly changing global market.

The window for such strategic shifts is narrowing. As the global gasoline trade flows evolve, driven by regulatory pressures and market dynamics, ARA’s terminals must adapt swiftly. This adaptation could take various forms, from enhancing blending capabilities to align with stricter environmental standards, to diversifying into alternative energy sources or more advanced processing technologies.

Conclusion

In conclusion, the ARA gasoline blending terminals stand at a pivotal juncture. The interplay of regulatory changes, market shifts, and emerging competitors like the Dangote refinery is reshaping the industry’s landscape. ARA’s terminals must navigate these challenges with agility and foresight. The decisions made in the near term will not only determine their competitive standing but could also set the tone for the region’s role in the global energy market for years to come. The urgency of a strategic review and potential terminal repurposing cannot be overstated, as ARA seeks to maintain its relevance in an ever-evolving industry.