The European oil refining landscape is in flux as oil refineries either close, are being converted or ownership shifts away from oil majors to new private equity players. Still, these assets are important to oil traders. Trading skills are core to the extraction of the full value of oil refineries and give oil traders optionality to trade around. New market participants joining the market often underestimate the complexity of asset-backed trading portfolios and don’t have the necessary trading capabilities and either must develop these capabilities or depend on third parties such as oil majors and large trading houses to provide these services through supply and offtake agreements. Supply and offtake agreements give the oil majors and major traders the benefit of having an asset to trade around without the risk and exposure of operating a complex industrial asset and the associated liability.

Asset-backed trading in oil has been at the core of oil majors and large trading houses’ strategy

Oil refineries give oil traders flow and a reason to be in the market: an entry to the game and a calling card to talk to other oil traders and other market participants up and down the value chain. A production asset gives an oil trader a position (e.g. oil refineries are short crude and long oil products) and a transfer price from the asset to the trader (or an implied target from the “LP” oil refinery linear program), which provides a reference price for the oil traders to try to beat in the markets. The margin gained by the oil trader is either retained or shared with the team responsible for the operation of the asset. Additionally, the insight gleaned from being in the market provides valuable information and a platform for speculation and financial trading.

An experienced and competent oil refinery trading team will be able to derive extra margin and add commercial value to the oil refinery itself. They will have a deep understanding of the LP model, the logistics of tankage and import/export capabilities and an understanding of the asset as well as knowing markets well enough to find the best supply of crude oil and potential end users for the refinery’s oil products. The main levers to pull are around quality (choosing the best spec and blending with no giveaway), utilization (filling up all the units), time (storing in contango, pricing in crude oil and out oil products at the best time to optimize time-spread value versus cost of capital for holding inventory) and location (selling to the best priced region and trading around options to sell in different locations). In an oil major or large trader with a collection of oil refineries, experienced and competent traders and a strong balance sheet, the capability to derive the additional value is clear but for companies with a limited financial muscle and a single oil refinery there is not the scale and resources to justify an extensive operation. With just a single refinery a trader does not have much optionality in terms of crude purchasing power or flexibility to move cargoes between refineries nor scale of supply to justify taking up multiple different shorts, developing blending capability, take on time charters, expand storage capability and build linkages to new markets.

Source: Stratas Advisors

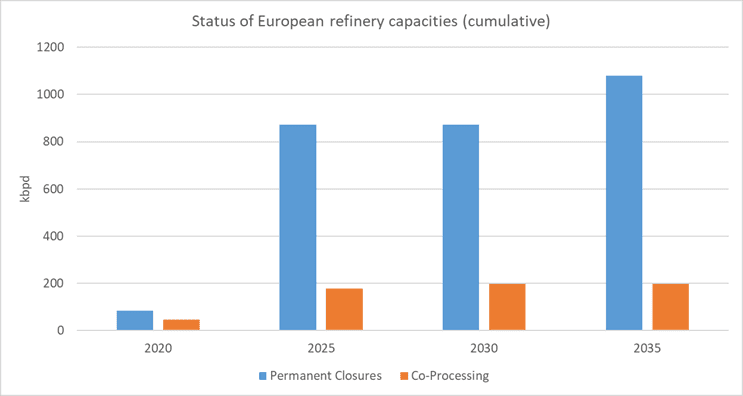

The refining landscape is changing

Since 2021 we have a collection of new market entries in the European refining space namely Crossbridge (Fredericia), Prax (Lindsey, Schwedt 37.5%), Liwathon (Miro 25%), G.O.I Energy (ISAB) and some are adding assets namely Klesch (added Kalundborg to Heide) and recently Entara (as operators of Fos). Private equity players have seen opportunities to grow their business where the oil majors have left. These smaller companies do not have the large trading capability nor the balance sheet that Equinor, Shell, Total, Exxon and Litasco had when they owned and traded around these oil refineries.

With oil majors selling off, closing and converting their oil refineries, their oil traders have less assets to trade around. 7% of refining capacity in Europe has been lost since 2020 and there are more planned closures coming. To name but a few examples, BP has just announced its partial closure of Gelsenkirchen and Petroineos are planning the shutdown of Grangemouth in 2025. Exxon just announced it will close Gravenchon chemicals plant, but has not the nearby Port Jeromé refinery. Shell has sold its share of PCK Schwedt refinery (and several US refineries recently), Preem are keen to sell their oil refineries, Irving has said they will consider selling or converting their Irish oil refinery Whitegate and oil majors are quietly trying to sell several others. Then there are sales driven by sanctions post war namely ISAB, JV refineries in Miro and PCK Schwedt. In addition there are the conversions to bio-diesel refineries where Nesté and Eni have led the way.

Some closed oil refineries are being converted to oil terminals (which avoids the environmental “clean-up” liability). An oil terminal still gives a trader a position in the market and provides tanks to blend and store in but does not have the same optionality as an oil refinery.

Major traders and oil majors are looking to grow their trading books by offering supply and offtake agreements to smaller refiners

In an attempt to fill the resulting reduction of assets in trading books of closed refineries, oil majors have been smart in retaining/adding oil refinery trading flows by offering the new owners the working capital financing that is required to purchase and hold the oil refinery inventory, which can be the bulk of the acquisition cost, as a “package” with the services of their oil trading teams to manage the supply and offtake agreements for a period of years. This still gives the oil trader an insight into what is going on in the region, flows to trade around and back stops for the crude oil they trade in the region without holding the crack risk, operational risk nor the liability or having the long-term exposure to declining demand. Growing traders such as Aramco, have also been hunting down supply and offtake agreements. Aramco have not been investing in oil refining in Europe, but they have rapidly, and impressively grown their book to trade products in Europe helped by deals with Motor Oil Hellas and Klesch. Oil traders, including traders with the oil majors, see value in still being able to trade around the oil refineries even if they don’t own them.

New companies currently don’t have the capability or experience to extract the full commercial optimization value from the refineries but the question is who will develop the internal capability (perhaps in partnership) to retain the trading value for themselves – like we saw Petroineos do with Morgan Stanley – remains to be seen. Much will depend on how much they need the support of third party for working capital financing as well as potentially utilising their credit lines (and margin funding) for trading and risk management.

Trafigura and Vitol have used some of their huge war chest, built up from record years of profits in the Covid and Post Covid market volatility, to invest in new assets. Trafigura have been active with their recent transactions of Fos in France and have supply offtake for ISAB. Vitol have their independent oil refining arm Varo (Cressier and 51.4% of Bayernoil) and are now in the process of buying Saras from Moratti family. Vitol and Trafigura have been competing for assets whilst other huge trader, Glencore, has not pursued the same strategy and stayed out of the arms race for now.

Oil traders will need assets that supply cleaner fuels to trade around

There is much activity in growing the supply of new cleaner fuels. We also see some steps to find new assets in biorefineries to trade around and would expect to see growth as we transition towards cleaner fuels. Shell is switching Rhineland to a biofuel operation. Nesté has lead the way in biofuels production. Eni have converted two of their refineries – Venice and Gela – to biorefineries and invested in biofuels production. Trafigura have just bought Greenergy, partly for the UK fuels market supply short and biofuels blending possibilities but also for its biofuel plants. Whilst projects in green ammonia, methanol, hydrogen and SAF are hard to get off the ground, and the economics are challenging, some are making it, and these will become the new assets to trade around. Will we see more of this kind of move into bio and hydrogen assets to give oil traders assets to lever into trading the new fuels around? Jet traders will want a SAF production – at a refinery or at a SAF plant to trade around. Gasoline and diesel traders want positions in biofuels– so yes that seems the likely way forward for oil traders to be prime buyers of these sites, either solely or as the “risk mitigator co-founder” with an institutional financing partner.

Fuel producing plants will still be at the heart of trading and the skills to optimize them are still the same. Asset backed trading is still the foundation of the leading majors and traders- and is here to stay. The product flows are beginning to shift away from owned refineries to bio and waste processing refineries, contracted supply offtake agreements with third parties and positions in terminals and wholesale markets. However, the opportunities to make money from trading the core concepts around quality spreads, location, time and utilization will always be there.

As the roles between asset owners and traders shift, there is still much to play for, with an array of challenges to consider, particularly for the newer market participants. At Energex Partners, we are well placed to support new and expanding companies throughout the process. With decades of practitioner experience from Morgan Stanley, BP, Shell and other leading players with backgrounds in oil, gas, LNG, biofuels, carbon capture and hydrogen, we support M&A transactions, and can set up and operate and monitor supply and offtake agreements, help build internal capability for the optimisation of assets and develop fit for purpose risk management policies and process. We can also support companies navigate the transition to trading new fuels, assessing where focus should be both in terms of asset investment and conversion and what models and trading strategies should be employed. We believe assets will always be important and we can help make sure they are properly evaluated, valued, optimised and traded.

Written by Liz Martin, Partner: lmartin@energex.partners.