Introduction

LNG shipping is increasingly an area of focus for certain infrastructure investors because of the favourable long-term growth fundamentals of the underlying commodity. In 2021 alone, three major deals were announced: the take private of Gaslog by BlackRock, Stonepeak’s acquisition of Teekay LNG and Morgan Stanley’s investment into Hoegh LNG Holdings. Deals with an older vintage (2019) include Cape Omega’s partnership with Knutsen and DIFs acquisition of equity shares in five newbuild carriers. Whilst each transaction had its own drivers, overall we see the sector as an attractive entry point for those with a strong sector conviction versus the much larger and more difficult-to-access liquefaction (US projects notwithstanding) and regasification segments.

The talk in infrastructure investing circles is that 2024 will see LNG shipping investments come to market and with this in mind, we outline below some of the potential risks that potential buyers should factor into their due diligence.

Market Snapshot

When approaching due diligence, investors need to be cognisant of certain trends within the vessel market that present both opportunity and risk. Overall there is a strong long-term growth story regarding LNG demand, though other structural risks remain:

The LNG market is growing and with it so is the number of vessels required: it is well known that a significant volume (130 mtpa+) is set to enter the market by 2026/7. With all this new LNG, must come the ships needed to transport it and net of the retirement of older ships, over 130 ships are expected to hit the water in the same time period. FIDs on the next wave of liquefaction projects that are targeting the re-opening of the supply/demand are already being taken and this will bring with it opportunities for new ship construction and also support recontracting. Shipbuilding is also driven in part by longer average journeys through cross-basin voyages, largely US Gulf to Asia.

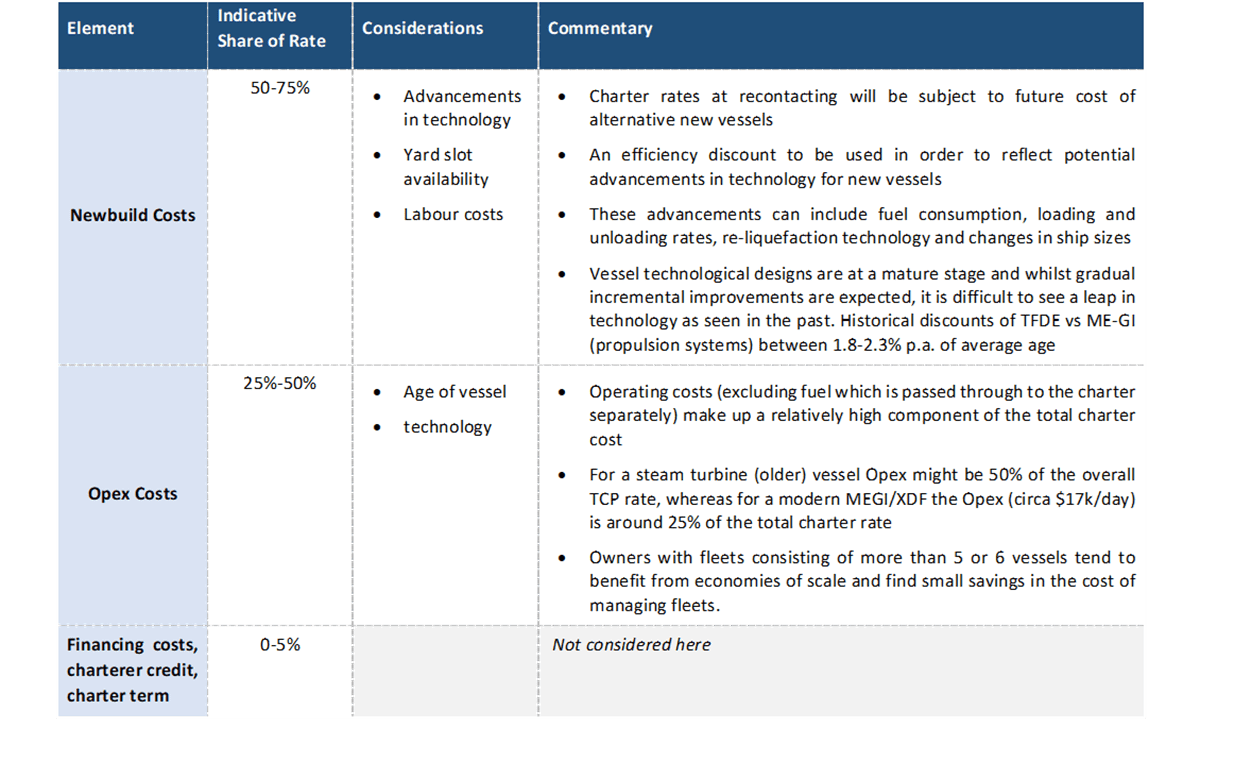

New build prices and therefore charter rates are staying at historic highs: providing support to long-term charter rates is the continued firmness in shipbuilding costs. As we cover below, new build costs are the main driver of term charter rates for new and existing vessels. Costs have always ebbed and flowed but following a COVID-19 slump, prices for a newbuild have been above $230mn and are currently at the $260m level. This compares to $193mn average between 2014 and Q1 2022. As an illustration of this pricing environment, a five-year old vessel recently transacted for $250 mn. This also demonstrates the other option to a long-term hold, which is to sell a vessel while it still has time to run on its charter to achieve a short-term return on capital.

Large capacity growth creates an oversupply and therefore charter rates risk in near-term: liquefaction projects coming on stream later than planned is not unheard of in the LNG business and is a lot more commonplace than late delivery of LNG ships; LNG ships constructed in a yard are much easier to build than a liquefaction project in a remote location. Therefore, the risk of a timing mismatch emerges with the LNG project delayed and the ships on time (or even early) and if this happens, the market could see an oversupplied vessel market. The knock on-effect for vessel owners is if this period coincides with recontracting of their vessels and impacts achievable charter rates.

Charter contracts are getting shorter: historically LNGCs were predominantly project-related investments with term charter rates attached. It was normal to see charters around 20 years in duration. With increasing market liquidity this average charter period has been eroded down to seven years on average, though we have seen charters attached for newbuilds of 12 years, which is seen as supportive for infrastructure style investments.

What do investors need to be aware of when performing due diligence?

Further to understanding high-level market dynamics, building a firm view on valuation will require a deep dive across key commercial issues. These will be based across two time horizons: at the time of purchase/when existing time charter parties are in force and then at the point of recontracting. There will also be important differences for newbuild ships that are in construction at the point of purchase that need to be considered.

Key terms of time charter party agreement(s) at point of acquisition

There will be limited/no scope to change the terms of the charter agreement for both operating and under construction ships and so investors will need to get comfortable with the terms as agreed. In addition to the term, charter rate and arrangements on Opex pass through, other terms to be carefully assessed as a potential owner:

Delivery terms for a newbuild ship: it is important to ensure that these are as close to back-to-back as possible with the ship building contract and that the majority of the liquidated damages remain with the owner.

Off-hire protection: this suspends the obligation to pay hire if the ship is prevented from performing the required services. If this can be extended beyond just planned maintenance then this will be at the benefit of the owner.

Taxes: what can or cannot be passed through to the charterer. With new environmental levies and taxes on shipping, owners should be aware if these are not able to be passed through.

Commercial relationship with the ship owner

The ship owner/manager will often retain a small equity stake in the vessel SPV – this provides an important incentive to drive performance and maintains the relationship with the charterer. The only risk is that the small equity stake incentivises the owner/manager to push profits and commissions into other areas of the project, e.g. project costs and yard supervision. This is not uncommon in the shipping industry. Such a risk is often mitigated by the importance of the relationship with the charterer that would suffer if this was carried out.

Charter rates at the point of recontracting

LNG ship investments can include a mixture of operating and in construction vessels. At some point, there will be a recontracting event and these will need to be assessed as part of any valuation. This might be under an extension option within the charter agreement (probably at an agreed rate) or with the ship going into the open market.

For investors, particularly those new to the sector, it is important to understand that charter rates are not something that can be forecasted based on market fundamentals. It is famously difficult to predict the behaviour of ship owners. The LNG industry is very cyclical with supply growth coming in “lumps” and demand side events can quickly change near-term shipping requirements that make forecasting very complex. If there is any guiding principle for charter rates it is newbuild costs and Opex, which are explained below.

The outlook for contracted revenues following the end of initial agreements

The other critical valuation assumption to consider at the end of the initial charter party agreement is how the vessel could be contracted in future. Whilst there could be an option exercised to extend, this will often only cover one or two new, shorter charter periods. For infrastructure investors with a need for long-term contracted revenues, assumptions need to be made on additional charters for the remainder of the vessel’s life – usually around 30 years. Charterer behaviour is driven in large part by a desire to contract for the newest most efficient ships with the lowest cost profile and so the older a ship gets, the harder it will be to secure long-term charters, when there are newer options out there. The other option would be to put the vessel to work in the spot market, which could be attractive if the market is tight and rates are high (spot rates can reach in excess of $300,000/day); this is however nearly impossible to predict more than perhaps 12 months out. Building realistic scenarios on vessel trading can help create bounds for contracted revenues for the vessel.

Conversion potential & the energy transition

The use of gas carriers is set to continue even as we transition away from fossil natural gas, be it CO2, H2 or e-fuels. This should create a case for conversions of LNGC’s so that useful life can be extended and with it, revenues. However, for both CO2 and H2, there is limited to scope to apply LNG tank design without such significant changes as to appear uneconomic. In the case of hydrogen, shipping in its liquid form is considered energy inefficient and costly, with the use of hydrogen carriers like ammonia preferred. The one exception is synthetic natural gas (or e-methane) that behaves like LNG and can use existing infrastructure; this technology is still in its infancy and therefore difficult to map its potential on to today’s LNG fleet. Therefore, unless significant technological breakthroughs take place, it should probably be assumed the vessels have a single ‘lifespan’.

Conclusion

The shipping sector is undoubtedly distinct from other midstream oil & gas sectors and this brings with it risk and reward. Investments are complex as they take place at the intersection of two different markets: physical LNG and shipping, with the latter less understood by the majority of infrastructure investors. For those who can build a strong investment thesis around recontracting, the sector could prove lucrative and a natural hedge against fixed assets with long-term stranded asset risk.

If you would like to know more about Energex work in LNG shipping and M&A advisory, please contact Tom Field at tfield@energex.partners or +44 7814990946