The announcement, in late November 2022, that Shell was to purchase 100% of Nature Energy Biogas A/S (Nature Energy) for nearly $2 billion capped off a year where biogas/biomethane had cemented itself as part of the mainstream gas industry and no longer a cottage industry taking place on isolated farms in rural parts of Europe. In purchasing Nature Energy, Shell joins BP and TotalEnergies in making bold moves into the sector; BP recently closed its purchase of Archaea Energy in the US and Total is currently seeking to close its purchase of PGB, which is based in Poland.

This transaction, and the high multiple of EBITDA paid by Shell, encapsulates the growing interest in the sector from both strategic and financial players. Nature Energy’s business bore out the strong investment thesis that has emerged for biomethane:

• Biomethane and anaerobic digestion represent a decarbonisation pathway for gas-consuming sectors – from grids to buses – that is available now using well-understood technology, in comparison to those yet to be commercially tested at scale, such as green hydrogen

• Strong demand for the molecules from gas suppliers in Europe who need to increase the renewable energy content of their portfolios, particularly in the transport sector and this allows for long-term contracts and the resulting stable revenue profile

• A strong tailwind of policy support in both the short and the longer-term; with the desire to decouple from Russian gas providing more immediate support and decarbonisation agendas creating long-term demand for green gas, which will be the final molecules to be displaced from the gas market in a Net Zero world

So where will the next Nature Energy come from? Currently, in Europe, there are no other directly comparable businesses and so if one is to emerge it will need to be built up. Either completely organically or through the rolling up of existing AD plants along with greenfield development.

If this is to happen, what key success factors of Nature Energy can be replicated and what are probably unique? To do this we have looked at how Nature Energy handles the most critical elements of the biomethane value chain: feedstock procurement and management to try and understand what developers and investors would need to replicate this success story.

Putting feedstock and its suppliers at the heart of the business model

With its first biomethane plant on stream in 2015, Nature Energy was ahead of its time in many ways but especially in its focus on animal waste as the backbone of its feedstock sourcing.

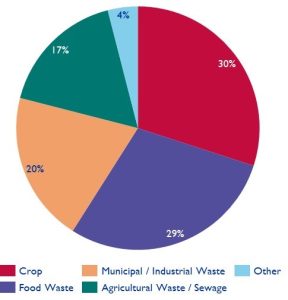

Today, waste from farm animals (cattle, pigs, chickens) is a vastly untapped resource for scaling up biomethane production in Europe. In the UK for example, it is estimated by the Anaerobic Digestion & Bioresources Association (ADBA) that in the UK alone, 2 Bcm of biomethane could be generated by animal wastes by 2030. For context, the UK currently produces around 0.8 Bcm of biomethane and 2 Bcm of biogas (i.e. gas not upgraded to biomethane) with crops and food waste the largest source of feedstock used in AD plants (producing biogas and biomethane, see figure below).

Figure One: UK AD Plants Feedstock Split (2020 data)[1]

[1] Source: UK Official Statistics, Department for Environment Food & Rural Affairs

From the beginning of Nature Energy’s biomethane operations, the business has been closely intertwined with the farming industry in Denmark, where there is a high proportion of pork and dairy farming. Plants have been developed with this feedstock in mind, including investment in required pre-treatment and a clear focus on building logistics chains that provide seamless operations for the farmers that drives adoption. This includes careful planning on how trucks drop off the waste and then pick up digestate (the by-product of an AD plant) and ensuring operations sync with seasonal changes.

A critical part of the Nature Energy business model is its use of a partnership approach with farmers in the plants it constructs. Typically, in each plant, a share of between 5-10% of the equity is provided to the farmers set to supply it with feedstock. This creates alignment and shared incentives for successful operations, as part of the focus on designing the facilities with the farmers in mind.

The focus on animal waste is then complemented by in-house capability in maximising gas yield through the addition of other waste types (like food or energy crops) when required. As a result, Nature Energy can point to a strong track record in delivery reliability that is then rewarded by long-term purchase agreements from buyers such as Shell.

The focus on feedstock procurement then allows for a key differentiator in the Nature Energy business model – large volume plants. Vidbaek, the largest in the Nature Energy portfolio can process up to 600,000 tonnes of waste per year (in the UK the average plant size is around 50,000 tonnes per year) which makes it one of the largest globally. This is enabled by high confidence in the feedstock supply but also by internal capability on design and construction using proprietary technology that drives important economies of scale. Nature Energy’s early history as part of a local gas company meant that its existing plants were connected to the gas grid, which meant the plants also had an existing route to market for their output.

How can this be replicated by new and existing players?

In building the leading European biomethane platform, Nature Energy was able to exploit some key leverage points. These include the high concentration of farms in Denmark and a first-mover advantage in building a network of feedstock suppliers. Additionally, Nature Energy benefited from very generous subsidy schemes in Denmark (effectively a feed-in tariff) as the country sought to build a leadership position in bioenergy. The Danish subsidy was unique in that it didn’t seek to limit the size of the plants, while most other subsidy regimes reduced the subsidy for larger plants which encouraged people to make them smaller.

Regardless of these, we see multiple opportunities in Europe for a platform biomethane business to connect farmers to AD plants and unleash the potential of animal waste.

To do so, developers need to:

• Be led by feedstock – establish your projects in areas with abundant supply and build strong relationships with farming co-operatives and associations to get to scale in supply quickly

• Understand critical details such as how different farmers currently collect waste and where the animals spend their time (indoors vs outdoors)

• Educate possible suppliers on the benefits of AD, such as the use of digestate as fertiliser

• Bake the needs of farmers into the design of the AD plant from inception, to drive towards frictionless operations that should support long-term partnerships

• Target large-scale plants, these will attract off-takers who would prefer to buy from single/few facilities and not multiple smaller plants

• Focus on sites that are close to the gas grid to ensure a route to market that is economic

• Build insight into the range of revenue generation options such as trading in carbon credits generated from production (or bringing a partner to help) or the possible sale of biogenic CO2 to those requiring it for the production of e-fuels, and construct a powerful story about the ability for plants to operate without subsidies through sales to the transport sector or corporate buyers. This can help access the large volume of infrastructure capital that is eager to grow exposure to the sector but needs to understand risks around terminal value

If forecasts for biomethane production under the RePowerEU are to be believed, we could be entering a golden age for the sector that will need innovative thinking, and capital and behavioural change. If that is the case, we will look back at Nature Energy as a catalyst for profound change.

Energex Partners draws on its experience of advising clients on waste-to-x projects, commercial issues across the gas value chain and infrastructure developments, when supporting investors and developers in the biomethane space. For more information, please contact Tom Field (tfield@energex.partners).

Article written by Tom Field.