Introduction

With its critical role as a fuel for heating homes and supplying power stations in an energy system that is increasingly tilting towards electrification, natural gas can be considered the lifeblood of the European economy. In this context, the replacement of Russian gas, severely reduced in the wake of the invasion of Ukraine, by LNG over the past 18 months has been the blood transfusion which has ensured the normal functioning of the economy.

While there have been some bumps along the way (momentous price spikes, infrastructure bottlenecks etc.), this fundamental shift has taken place with surprising efficiency overall, thanks mainly to the market’s evolution away from a limited ‘point-to-point’ model to one that is more flexibly traded, along with strategic decisions made at Government levels to install large amounts of regas capacity across the continent.

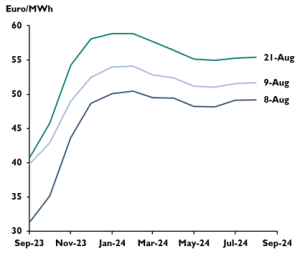

Behind this transition is the emergence of an important new consideration for gas buyers: the increasing exposure to global gas/LNG market dynamics through European wholesale prices. This has been powerfully underlined by the recent news of potential strikes by workers at three Australian LNG projects, which caused TTF prices to jump by around 27% on the 9th of August.

TTF Futures Forward Curve Evolution Across August 2023

Source: European Energy Exchange

The increased reliance on LNG in Europe demonstrates the need for gas buyers, as a no regret option, to develop analytical capabilities that cover global gas and LNG markets in order to understand how market events will drive pricing dynamics in European markets. We see the European net balance as a key market indicator that participants can use to map the impacts of certain market events or shocks.

A new fragility within Europe’s gas market

Despite its distance from Europe and the fact that none of the at-risk Australian production would likely find its way to consumers there (as it is contracted to flow to Asia), the need for Asia to satisfy inelastic gas demand has triggered fears of a ‘battle’ for spot volumes with European buyers. This has spooked markets and demonstrates the greater fragility of the global LNG supply market that now needs to provide baseload volumes to both Asia and Europe.

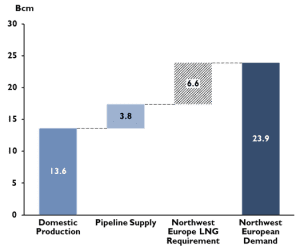

Using the Energex LNG and Gas Model (LGM) we have modelled the short-term net balance of Northwest Europe and results point to a finely balanced market at present, moving into undersupply and a need for greater LNG volumes over the coming winter. Looking at October 2023 as an example, our forecasting suggests that approximately 6.6 Bcm of LNG is needed to balance the market. This requirement increases sharply moving deeper into winter, hence the short-term contango in the forward curve this winter.

Northwest European Gas Supply Mix, October 2023

Source: Eurostat, Energex analysis

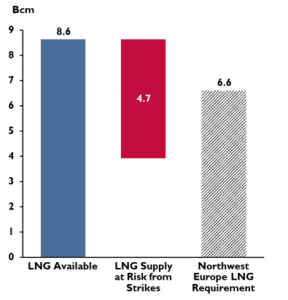

Any further supply shocks, or demand spikes, will exacerbate pricing levels in an already volatile market. For example, if strikes were to take place in Australia at the Gorgon LNG, North West Shelf and Wheatstone LNG facilities during October, this would remove up to 4.7 Bcm of LNG from the market which Asian buyers in particular would seek to replace from the spot market. Our model forecasts 8.6 Bcm of LNG available for Northwest Europe in October, of which 6.6 Bcm is required. Increased competition for over half of this volume would lead to much tighter dynamics, increased volatility and higher outright prices.

Northwest European LNG Requirement vs. At-Risk Supply, October 2023

Source: Stratas Advisors, Eurostat, Energex analysis

Conclusions

LNG imports accounted for 42% of EU 27 total gas supply in the first half of 2023 and the connection with other parts of the global market is only going to strengthen given the on-going build out of regas capacity. This brings the benefit of more flexible volume to balance the market but also its drawbacks for end users in terms of increased volatility and the need for a more robust approach to risk management.

Understanding the possible changes in the net balance can help gas buyers understand what could cause this volatility, inform procurement decisions and shape risk management.

Recognising the time required to build these kinds of analytical tools in house and the challenges involved in the recruitment of analysts to manage analytics (especially in locations outside of key hubs like London), we are supporting our clients, backed by the use of the Energex LGM to run multiple scenarios on supply and demand, to inform approaches on optimum market participation and risk management strategies.