The economic landscape in energy markets is increasingly defined by the value attributed to products with lower intensity of greenhouse gas (GHG) emissions as the energy transition accelerates and governments increase direct regulations and policies.

The LNG industry, with its largest phase of growth still set to take place in a market increasingly shaped by decarbonization efforts1, will also see a shift in its economics. This article looks at the value drivers in low-emission LNG and the potential impacts and strategies for LNG market participants across the value chain.

Regulations and Voluntary targets will drive the value in low-emissions LNG

The value of low- emission LNG is driven in two key ways:

1. The development of direct regulations and import levies

- EU Methane regulation – set to impose a limit on the methane-intensity of fossil fuel imports; there is however no clarity yet on how this limit will be set or how emissions will be monitored and verified

- Japan is set to introduce a carbon levy on fossil fuel imports from April 20282 onwards

- EU Carbon Border Adjustment Mechanism (CBAM) – currently excludes pipeline gas and LNG imports but there is a risk of further scope inclusion

2. The impact of voluntary targets

- All the largest LNG market players have set emissions reductions targets under pressure by investors and governments

- Investors and lenders are also increasingly factoring the emissions intensity of projects as a key part of their assessment of their commercial viability, in part due to their own decarbonization commitments

However, while the emergence of these value drivers point towards a potential premium for low-emission intensity LNG, this remains at present mostly speculative or only linked to long-term targets. This lack of clarity on value and associated payback mechanisms make investment decisions especially challenging regarding the management of Scope 1 and 2 emissions of LNG.

The value of low-emissions intensity LNG will reshape the market

The emergence of a value associated with low-emissions LNG will change the relative competitiveness of cargoes and affect value chain economics. This will impact three key aspects: market prices, the value of legacy assets and contractual dynamics.

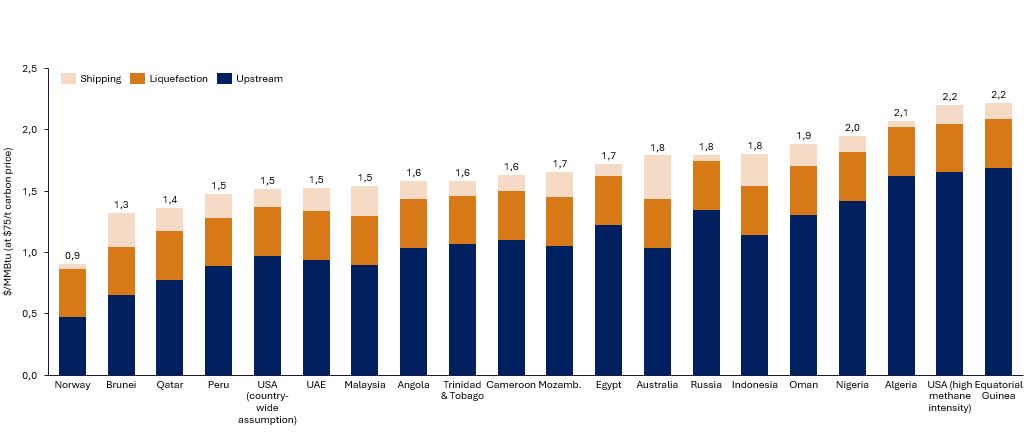

An example analysis of the potential impact on market prices is provided in Figure 1 below, which shows the economic impact of a border CO2e emissions tax on LNG supply to Europe. This illustrates the magnitude of the direct economic impact that the pricing of emissions intensity would have on the LNG market.

Figure 1 – Impact of a border CO2e emissions tax for LNG supply to Europe from key exporting countries3

The second key impact of such a change in the relative value of LNG would be on the long-term value of infrastructure assets. For example, in a scenario that the LNG market peaks and enters its long-term decline, a sufficiently high level of carbon taxes would significantly affect the expected lifetime of legacy assets producing LNG from fields with high emissions, with some that would have otherwise been considered resilient to market fluctuations potentially rapidly becoming uneconomic to operate. Alternatively, if demand is sufficiently robust some export projects may be limited to only delivering to markets that do not apply a penalty to higher intensity LNG, effectively operating in a separate and lower-price market.

Finally, contractual dynamics will be impacted as, while many LNG contracts have clauses accounting for such changes in law, the change in the commercial balance will be significant and may lead to challenging renegotiations. In this area, the key questions to be addressed by LNG sellers and buyers are:

- For legacy contracts, especially DES agreements, which contractual party would take liability for any future taxes imposed on imports?

- Can price review clauses be activated based on such a change in law in the end market?

- For new contracts, which party is best placed to manage risks and opportunities coming from these developments? How does it change the risk-reward balance between the parties?

- Will there be a further increase in FOB contracts signed as destination flexibility for buyers becomes increasingly important for portfolio optimisation if the pricing of emissions vary widely across key LNG markets?

- In a buyers’ market, for example, would sellers be willing to commit to a maximum emissions-intensity level in SPAs?

Mitigation actions that carry limited risks are becoming the norm, not the exception

Faced with these potentially significant impacts, many market participants are already acting to reduce their Scope 1 and 2 emissions. These have, however, generally been actions that have a minimal impact on a project’s economics or already have a business case.

Of these, the most common move to date has been to increase the process efficiency and the electrification of the liquefaction process, which generally accounts for ca. 25% of the Scope 1 and 2 emissions of LNG.

There are also multiple projects seeking to reduce upstream emissions via CCS. However, these are generally located in jurisdictions with active economic incentives for emissions reduction (e.g. USA and Canada) or that seek to develop international CCS hubs (e.g. Middle East and South-East Asia). CCS as part of reducing CO2 content in upstream gas for LNG can be an important enabler for domestic CCS industries through provision of anchor volumes for storage projects, creating a virtuous circle.

These market developments are also likely to further incentivize any improvement in process efficiency available to legacy LNG projects, although at present, without direct economic incentives, these are likely to continue being driven by a focus on lower costs and higher production.

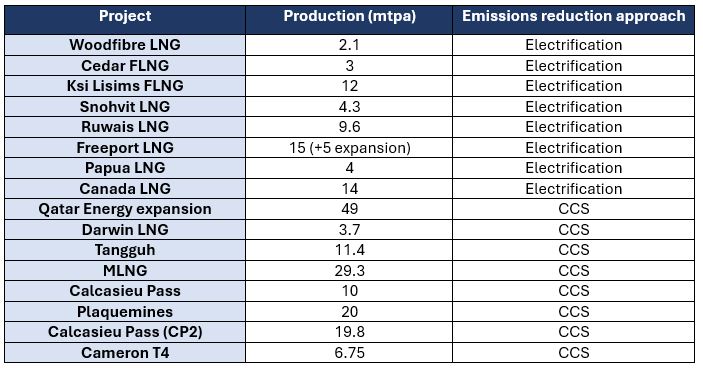

The result is that there are already almost 230 mtpa worth of LNG either operational or planned that include a significant reduction in emissions intensity (a selection of which is shown in Table 1). Such plans have in fact become so widespread now that they have become the norm, not the exception, and investors, lenders and LNG buyers are coming to expect them in pre-FID projects.

Table 1 – Operational or planned LNG projects with emissions mitigation measures4

Key takeaways

The potential emergence of a differential in value being applied to LNG cargoes based on their carbon emissions is now a risk that must be accounted for by market participants. In this context, market participants should:

- Understand how regulations and policies will affect markets in which they operate, assessing the risk and impact of potential future developments

- Ensure clear and reliable methodologies are in place, preferably in line with an independent body, to measure and monitor emissions from own operations or third-party gas or power suppliers

- Identify what is achievable based on location, market view and operational capability and take actions that lead to emission mitigation:

- Improve efficiency across LNG value chain, e.g. process optimisation and waste heat recovery

- The electrification of liquefaction for new projects

- Deployment of CCS leveraging existing incentives or where LNG related upstream CCS can be an enabler for a broader industry

- Further actions that might include LNG contract modifications or capital investments in new or upgraded lower emissions infrastructure (especially for older assets) can be taken. Marketing strategies may also need to be updated to account for the risk of changes in border carbon taxation in end markets. The cost of these actions should be weighed against a careful assessment of the magnitude and likelihood of potential risks, in order to assess if and when to act.

- Finally, if such actions are not possible, focus can be shifted to other competitive advantages to ensure resilience against these changes, such as minimisation of costs or more flexible commercial models (for example smaller-scale projects offering shorter contracts).

1 The Shell LNG Outlook 2024 projects a market growth of 35%-50% by 2030 compared to 2023

2 This plan is part of Japan’s “GX Promotion Act” enacted in May 2023

3 Energex analysis of Global Registry of Fossil Fuels data

4 Source: IGU World LNG Report – 2024 Edition (with additions by author)

Written by Rui Almeida, Partner: rfalmeida@energex.partners and Giovanni Bettinelli, Senior Advisor: gbettinelli@energex.partners