With much discussion around Sustainable Aviation Fuel (SAF) as a viable pathway to decarbonise the aviation industry, Dentons and Energex Partners have collaborated to analyse the legal and commercial aspects of the regulatory landscape for SAFs, and how industry can navigate these issues.

1. Introduction: Why is everyone talking about SAF?

As we progress closer to various decarbonisation targets, aviation has attracted particular scrutiny from regulators and policymakers given that: (a) it accounts for approximately 2.5% of global CO2 emissions; (b) air travel is projected to continue to increase significantly over the coming decades; and (c) the general public and businesses are becoming more considerate of their carbon footprint when travelling, although this is without the full reality of possible price rises being factored in.

There have recently been a number of significant developments in efforts to accelerate decarbonisation of the aviation sector, notably in the area of Sustainable Aviation Fuel (SAF). In 2021, member airlines of the International Air Transport Association (IATA) passed a resolution with a commitment to reach net zero carbon emissions from operations by 2050, with SAF playing a pivotal role in achieving that target. At an EU level, EU legislation including RED III, the ReFuelEU Aviation Regulation[1] and the European Union Emissions Trading System (ETS)[2] all seek to drive the decarbonisation of this carbon intensive sector by, amongst other things, mandating and encouraging the production and use of SAF in the EU.[3] We discuss these core pieces of legislation below and their implications for the aviation sector.

SAF production has therefore become a topic of much discussion in the aviation industry and amongst fuel suppliers as market participants seek to upscale the production and use of SAF whilst grappling with the complexity of the legislative requirements, and the challenges and costs, that come with the development of first-mover projects in a market that remains in its infancy.

2. What is SAF?

SAF is a “drop-in”[4] fuel, meaning that it can be blended with conventional jet fuel in order to reduce the carbon intensity of the aircraft’s fuel batch. It can be safely used by all aircraft and engines that are certified to operate with jet fuel (i.e. SAF can already be used in the majority of operational aircraft). Whilst SAF still contains carbon, and therefore still emits CO2 into the atmosphere when it is combusted, if the SAF is produced using certain sustainable pathways, it is not considered to be as carbon-intensive as conventional jet fuels and therefore: (a) reduces the carbon emissions accounted for in the plane journey; and (b) enables the fuel usage to contribute to meeting the mandated targets, such as those set out in the ReFuelEU Aviation Regulation and RED III, or under CORSIA, which are set out in section 3 of this article.

The International Civil Aviation Authority (ICAO) defines SAF as “a renewable or waste-derived aviation fuel that meets sustainability criteria”. However, the exact “sustainability criteria” depend on where and under which jurisdiction or regulation the fuel is ultimately intended to be used as we will explore further in this article.

Under European regulation (explored in greater detail below), to be considered as “SAF”[5] the fuel must fall into one of the following categories, which reflects the different production pathways:

(a) an aviation biofuel, being fuel that is:

-

- a “biofuel” i.e. liquid fuel produced from a prescribed biomass feedstock such as cooking oil, unintentionally damaged crops and municipal waste water;

- an “advanced biofuel” being liquid fuel produced from a prescribed biomass feedstock such as animal manure and sludge, palm oil mill effluent, nutshells, cobs cleaned of corn kernels and biomass fraction of waste; or

- “biofuels” produced from any other biomass source excluding food and feed crops;[6]

(b) a synthetic aviation fuel, or e-fuel, being fuels made by synthesising green hydrogen with captured CO2, that fulfil the criteria for renewable fuels of non-biological origin (RFNBO) under RED III (e.g. e-SAF);[7] or

(c) a recycled carbon aviation fuel, being a fuel produced from waste streams of non-renewable origin that meets the requirements of RED III (e.g. jet fuel made from synthetic crude oil derived from municipal solid waste).

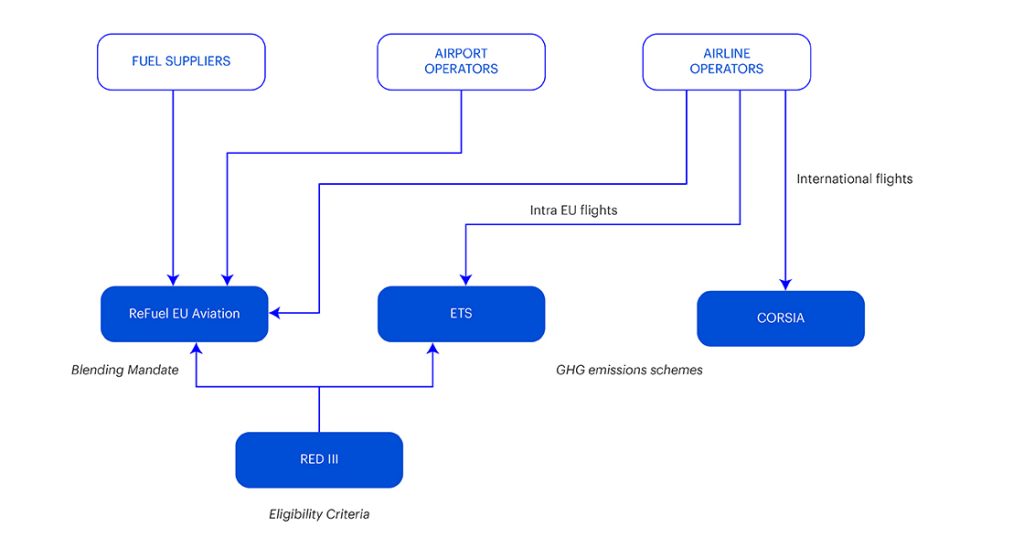

3. Regulatory framework for SAF in the EU

The core pieces of EU legislation that need to be grappled with by the SAF industry are summarised below, with the interplay between them depicted in the schematic.

SAF regulatory framework impacting EU

(a) RED III and the Delegated Acts

RED III is the backbone of the EU’s decarbonisation legislation and sets overarching targets for the use of renewable fuels across numerous sectors in the EU. For aviation, the RED III sub-targets are further developed by the subsidiary ReFuelEU Aviation Regulation, discussed below.[8] Of particular relevance to SAF is the sustainability criteria which applies to the production process (in any of the categories above) for fuels seeking to qualify as SAF (in particular, for RFNBOs, through the hotly debated Delegated Acts).[9] This includes strict limitations on the eligible sources of (a) renewable electricity and (b) captured CO2 used in the production of RFNBOs.

(b) ReFuelEU Aviation Regulation

The ReFuelEU Aviation Regulation supports the achievement of the RED III targets through aviation-specific measures, recognising the more expensive production costs of jet fuels relative to other transport modes. The regulation places specific SAF usage (or blending) obligations on aviation fuel suppliers, certain aircraft operators[10] and EU airports.[11] Specifically:

-

- fuel supplied by aviation fuel suppliers to aircraft operators at EU airports must contain an average minimum SAF share, starting at 2% from 1 January 2025, rising to 6% by 2030 and thereafter in increments to 70% by 2050;

- such SAF should contain a minimum amount of RFNBO, with a sub-target of 1.2% required by 2030 rising in increments to 28% by 2050;

- applicable aircraft operators are required to uplift at least 90% of their annual fuel requirements from an EU airport (to avoid tankering at airports outside the EU to avoid lifting the more expensive SAF-blended kerosene); and

- airport managing bodies[12] to facilitate access to aviation fuel containing the minimum SAF blend (this may include, for example, having the required infrastructure for SAF storage and transmission to aircraft).

Various reporting obligations apply to aircraft operators and fuel suppliers in the EU to monitor compliance. In the event that the regulation is not complied with, member states are mandated to impose fines.

The regulation establishes minimum thresholds for fines imposed by member states for failure to comply with the above. The severest penalties apply for failure to supply minimum SAF amounts in accordance with (i) and (ii) above. Culpable fuel suppliers are liable to: (a) pay a penalty of twice the amount of the difference between the conventional Jet A1 price and SAF price multiplied by the shortfall amount; and (b) make up the supply obligation in the following reporting year. In raw economic terms, this could amount to penalties of €4,000 per metric tonne (p/mt) for bio-SAF and €8,000-16,000 p/mt for e-SAF (based on market pricing forecasts).[13]

The ReFuelEU Aviation Regulation must be read together with RED III given that RED III ultimately dictates what fuels qualify as SAF and which fuels can therefore be accounted for in ascertaining whether the mandates are being met.

It is worth noting that many airlines have set voluntary targets that are above those mandated under RED III (e.g. 10% by 2030 vs. 6%). While Europe is currently seeing an oversupply in SAF as a result of large inflows of Asian biofuels, this is expected to dissipate by 2026. In the longer term, it will be challenging to meet these targets as new supply capacity faces regulatory uncertainty and struggles to compete on price, making it possible that the market will be sized by production capacity more than the regulatory targets.

(c) ETS

The European Union Emissions Trading System (ETS)[14] sets a limit on CO2 emissions for certain industries, including for the aviation sector in respect of certain flights between EU airports. Whilst the ETS currently only applies to internal flights within the EU, prior to 1 July 2026, the European Commission is mandated to submit a report and legislative proposal (if required) to assess the adequacy of CORSIA (see below) in relation to achieving the goals of the Paris Agreement. This review may result in the application of the ETS being extended to apply to international flights departing from the EEA.

ETS targets the aircraft operators, requiring them to surrender sufficient carbon “allowances” to cover their emissions. Under the system the “cap” of allowances is determined on an annual basis by the European Commission (and will decrease over time) and is allocated to member states. Whilst a certain proportion of such allowances is currently allocated to the aviation sector for free, this free allocation is intended to be phased out by 2026 (subject to point (ii) below), after which all allowances will be auctioned.

The ETS encourages the use of SAF by aircraft operators by:

-

- applying an emission factor of zero to SAF meaning that no ETS allowances are required to be surrendered against the SAF portion of aviation fuel (reducing the overall carbon tax exposure); and

- providing 20 million free allowances to commercial aircraft operators using SAF between 1 January 2024 and 31 December 2030.

Regulatory framework for SAF under CORSIA

Separate to the legislation and targets implemented by the EU, which currently apply only to internal flights between EU member states, the aviation sector has devised and is in the process of implementing the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA). CORSIA will apply to all international flights between member countries of the ICAO (i.e. flights between non-EEA states and between an EEA state and a non-EEA state) and therefore has potentially far broader implications for the wider aviation sector.

CORSIA is a market-based mechanism specifically for the aviation sector and is the first of its kind globally. The mechanism requires airline operators to utilise ICAO-approved carbon credits (CORSIA Credits) to offset a portion of their verified emissions for a given compliance period. The offsetting requirements of aviation operators can, however, be reduced through the utilisation of certain sustainable and low carbon aviation fuels (Corsia Eligible Fuels or CEFs).

These CEFs are Sustainable Aviation Fuels, similar to those mandated by the EU. However, the sustainability requirements of these CEFs and, in particular, the minimum lifecycle GHG savings threshold, differ from those set out in the RED III. Under CORSIA, the ICAO Council sets the sustainability criteria for CEFs and approves sustainability certification schemes to ensure compliance with the mandated sustainability criteria.

Once airline operators have reduced emissions through technological and operational improvements and through the utilisation of SAF/CEF, they are required to offset a portion of their remaining emissions using CORSIA Credits.

CORSIA is now entering its first full implementation phase in 2024, following the end of the pilot phase which lasted from 2021 to 2023. Compliance with the scheme for aircraft operators in the approximately 129 jurisdictions that have signed up to CORSIA is currently voluntary, but will become mandatory for all ICAO states from 2027. Airline operators of impacted states and flights must take the appropriate steps to ensure compliance, through procurement of CEFs and CORSIA Credits.

However, CORSIA is a nascent market and a number of significant uncertainties remain yet to be resolved. Most significantly, the first full phase of CORSIA, effective 2024, sees a significant change in the types of carbon credits that may be eligible for the scheme and supply has been materially reduced from the pilot phase. The price of CORSIA Credits and potential future supply is therefore currently a significant unknown. As the CORSIA market evolves and matures, the price at which airline operators are prepared to substitute CEFs for CORSIA Credits, and vice versa, will become clear and this has the potential to be a significant source of CEF/SAF demand going forward.

4. Regulatory complexity as barrier to development

Slow ramp-up in regulatory schemes

The proposed and existing SAF blending mandates and the potential demand from airline operators under existing and emerging carbon compliance markets will require rapid scaling of SAF supply in the coming years. However, given the slow development of the regulatory landscape, achieving these early targets could prove to be a challenge. The regulatory certainty which is required to encourage investment at the scale required in the sector has, to date, been largely lacking and the necessary clarifications to pieces of regulation and legislation have been delayed. ReFuelEU Aviation is due to be reviewed in 2027, which has created hesitancy among affected market participants to be a “first mover” and incur the SAF premium only to see the goalposts be moved in the review in response to the forecast SAF shortage.

Furthermore, the specific RED III requirements on the production of RFNBOs are stringent, such as the proposed requirement for co-location and additionality of renewable electricity installations for green hydrogen production plants, and the required temporal correlation between renewable electricity generation and H2 production, both of which will lead to significantly higher costs in the production process.

Necessary infrastructure, such as the EU Union Database, the registry system that records and traces the necessary sustainability criteria for biofuels and feedstocks, has only become operational in 2024 and is only recently being utilised.

Meanwhile, CORSIA has been significantly impacted and delayed by the COVID-19 pandemic. The original emissions baseline year of 2019 has been reset following the grounding of the sector during the COVID-19 period and a new baseline has had to be established as a starting point for emission reductions. Furthermore, the eligibility of CORSIA Credits into the system has been, and remains, a significant unknown. Numerous factors have contributed to the uncertainty surrounding eligible credit standards and methodologies, some of which are yet to be resolved. This uncertainty has delayed the market development of phase 1 CORSIA Credits, which in turn raises uncertainty over demand for CEFs and delayed a clear market price signal.

This regulatory uncertainty has contributed to a lack of willing counterparties to enter into long-term offtake agreements and has potentially stalled the development of the market, which in turn has served to delay investment decisions.

Regulatory risk and changes to sustainability criteria

As mentioned previously, different markets and jurisdictions, such as the EU and the CORSIA system, may apply different sustainability criteria to what qualifies as SAF, in particular with regard to the feedstocks which are eligible for use in production. Producers therefore must await clarity on regulation before determining which market to sell into, taking into account where there is most value for their product or where sustainability criteria may be more favourable. Furthermore, sustainability criteria in some jurisdictions may become more stringent over time, making compliance with this requirement more difficult and potentially removing some of the early supply from the market. Clarity on sustainability criteria in the EU and CORSIA markets, and any other jurisdictions where regulation is driving demand for SAF, is a key enabler of the market and a key determinant of supply availability.

Competition with other sources of regulation-driven demand

Demand for the same feedstocks that are used to create SAF is being stimulated by other regulation and developing markets. For example, other elements of the EU “Fit for 55” package, such as RED III targets for adoption of renewable fuels in transport, and FuelEU Maritime regulation in Europe, mandates certain “well to wake” emission reduction criteria for the maritime transport sector. These targets will encourage competing demand for the same feedstocks that can be used to generate SAF and may therefore constrain supply for SAF production.

Conclusions and implications

As we have discussed above, a number of regulatory initiatives to drive decarbonisation in the aviation sector have entered into force, or will be doing so in the near future. As one of the most difficult sectors to decarbonise, SAF will play a critical role in this decarbonisation effort. Demand for SAF, therefore, should be significant in the years to come, as more countries and jurisdictions impose SAF blending mandates, carbon pricing systems become more onerous and CORSIA moves towards mandatory implementation for ICAO member states.

Implications for producers

The various imminent regulatory drivers suggest that there will be a strong and sustained demand for many kinds of SAF going forward. Producers will need to consider what type of SAF they should be producing and which market they should be targeting, based on the sustainability criteria and prevailing market price for SAF under each regulatory mechanism. This will, to a large extent, depend on the availability of suitable feedstocks and ability to evidence sustainability requirements. For example, producers aiming to target the European SAF market will need to satisfy the requirements of RED III and evidence sustainability criteria via the Union Database and the price paid by the European market (driven by the blending mandates) will need to be sufficient to cover such costs. Similarly, producers aiming to target the wider CORSIA market will need to satisfy the CORSIA requirements as set out by the ICAO Council. It will be possible, of course, for certain SAF to qualify for several regulatory schemes and therefore attract the highest price.

However, the price and availability of qualifying feedstocks remains a significant factor for producers. With limited ability to hedge against volatile feedstock price movements and limited availability of long-term offtake, producers currently have little certainty and are therefore themselves unable to commit to long-term supply agreements.

It is likely that these markets will evolve at differing speeds and some markets will have more transparency than others in terms of pricing. Furthermore, these regulatory requirements will evolve over time and sustainability criteria may become more stringent. Producers therefore need to plan carefully how they will adapt to these evolving requirements.

Implications for project financing of SAF projects

Lenders providing limited recourse project financing to SAF production plants will want to ensure that the producer is insulated from regulatory risks. Ideally, the costs of compliance with a change in regulatory requirements should be passed through to the offtaker (SAF customer) under the offtake contract. Regulators could assist the market by providing assurances around “grandfathering” of first-mover projects (shielding them from compliance with future tightening of criteria). Distinction should be drawn with changes in the laws of the host country where the SAF is produced, particularly an emerging market, which will usually not be borne by offtakers and should ideally from a financing perspective be allocated to the host government where the project is being developed under a concession. Where producers are seeking to avail themselves of the flexibility of targeting different markets (i.e. without the full output being contracted to a single offtaker), lenders are likely to require a detailed marketing analysis and agree an offtake strategy as part of the financing requirements.

Implications for traders

The nuances of different regulations across jurisdictions will create opportunities for traders who can understand how they fit together and potentially overlap. The opportunities for regulatory arbitrage will present themselves as legislation evolves and as SAF markets take shape. Similarly, demand for a long-term and secure supply of SAF from airline operators should provide traders with multiple possibilities to establish “short” positions, from which they can build potentially profitable trading businesses and take advantage of market dislocations and inefficiencies. Furthermore, nascent markets frequently provide opportunities that more mature markets do not, as opportunities for traders often dissipate over time, as markets become more efficient and opportunities for arbitrage decline. The nascent SAF market is likely to be of significant interest to experienced traders.

Implications for airlines

Airline operators may find they have limited alternatives to meet the various compliance requirements under the emerging systems. Where a compliance mechanism does have a degree of flexibility, such as under CORSIA, where certain carbon credits can be used to offset emissions and meet targets, airline operators may look to develop such alternatives as part of their procurement and hedging strategies in place of SAF. Given the current high prices of SAF, this should in theory translate into strong demand and an equivalent price for such credits. Almost certainly, this will be significantly higher than the prices seen in the voluntary carbon market today.

Similarly, under the EU ETS, airline operators can purchase carbon allowances (EUAs) to meet their ETS compliance obligation and pay for their emissions for flights within the EU. The use of SAF can reduce this obligation, but is unlikely to be widely adopted in the short term, given the current price of SAF relative to the market price of EUAs. Without the blending mandates imposed by ReFuelEU Aviation, it would require a materially higher EUA price than the current market to incentivise widespread SAF adoption in the EU and/or a much higher penalty for failure to surrender sufficient allowances.

This article was authored by Colm Ó hUiginn, partner, and Claire Hunter, senior associate, in the Projects team at Dentons; and Michael Fulton, Head of Carbon, and Tom Field, Head of Gas & LNG at Energex Partners.

If you would like to understand more, please contact Michael Fulton mfulton@energex.partners or Tom Field tfield@energex.partners at Energex Partners.

[1] Regulation (EU) 2023/2405 of the European Parliament and of the Council of 18 October 2023 on ensuring a level playing field for sustainable air transport (ReFuelEU Aviation).

[2] Directive 2003/87/EC of the European Parliament and of the Council of 13 October 2003 establishing a system for greenhouse gas emission allowance trading within the Union and amending Council Directive 96/61/EC (Text with EEA relevance).

[3] The ReFuelEU Maritime Regulation (Regulation (EU) 2023/1805 of the European Parliament and of the Council of 13 September 2023 on the use of renewable and low-carbon fuels in maritime transport, and amending Directive 2009/16/EC) also includes similar obligations with respect to the maritime industry. However, this article is focused on SAF and therefore aviation.

[4] They are chemically and functionally the same as the conventional fuel they are replacing, hence they are synthetic fuels and can be dropped in without any extensive modification required to the engine.

[5] Sustainable Aviation Fuel and associated definitions are set out in the ReFuelEU Aviation Regulation, which cross-refers to RED III criteria.

[6] Food and Feed Crops are starch-rich crops, sugar crops or oil crops produced on agricultural land as a main crop excluding residues, waste or ligno-cellulosic material and intermediate crops, such as catch crops and cover crops, provided that the use of such intermediate crops does not trigger demand for additional land.

[7] Generally speaking, RFNBOs are green hydrogen and its derivative products. i.e. renewable electricity that is used to separate water to produce hydrogen which can be further synthesised with other chemicals, such as CO2 to produce e-fuels. Refer to Dentons’ article which discusses the regulatory criteria to be met for RFNBO production: “When is H2 = RFNBO? Renewable hydrogen and ‘green’ e-fuels in the EU (Part 1)” https://www.globalenergyblog.com/when-is-h2-rfnbo-renewable-hydrogen-and-green-e-fuels-in-the-eu-part-1/. Please also refer to Dentons’ third article which discusses the eligible sources of CO2 that can be used in RFNBO production: “Avoided CO2 emissions – Renewable hydrogen and ‘green’ e-fuels in the EU (Part 3)” https://www.globalenergyblog.com/avoided-co2-emissions-renewable-hydrogen-and-green-e-fuels-in-the-eu-part3/.

[8] Targets include:

- at least 29% of the energy consumed in the transport sector in the EU is from renewable sources (or that there is reduction in the greenhouse gas intensity of the transport sector by at least 14.5% by 2030); and

- the combined share of: (1) advanced biofuels and biogas produced from certain listed feedstocks of biological origin; and (2) RFNBOs, in the energy supplied to the transport sector in the EU is at least 1% in 2025 and 5.5% in 2030 (with a minimum, of which 1% should be from RFNBOs in 2030).

[9] Commission Delegated Regulation (EU) 2023/1184 of 10 February 2023 supplementing Directive (EU) 2018/2001 of the European Parliament and of the Council by establishing a Union methodology setting out detailed rules for the production of RFNBOs. Commission Delegated Regulation (EU) 2023/1185 of 10 February 2023 supplementing Directive (EU) 2018/2001 of the European Parliament and of the Council by establishing a minimum threshold for greenhouse gas emissions savings of recycled carbon fuels and by specifying a methodology for assessing greenhouse gas emissions savings from RFNBOs and from recycled carbon fuels.

[10] The regulation applies to aircraft operators who operated at least 500 commercial passenger flights, or 52 commercial cargo flights, departing from EU airports in the previous reporting period (or, where that person cannot be identified, the owner of the aircraft).

[11] The regulation applies to airports in the EU where passenger traffic was greater than 800,000 passengers or where freight traffic is higher than 100,000 tonnes in the previous reporting period.

[12] A body which administers and manages the airport or airport network infrastructures and coordinates and controls the activities of the different operators present in the airport or airport network concerned.

[13] https://www.transportenvironment.org/articles/implementing-the-eus-e-saf-mandate.

[14] Directive 2003/87/EC of the European Parliament and of the Council of 13 October 2003 establishing a system for greenhouse gas emission allowance trading within the Union and amending Council Directive 96/61/EC (Text with EEA relevance).