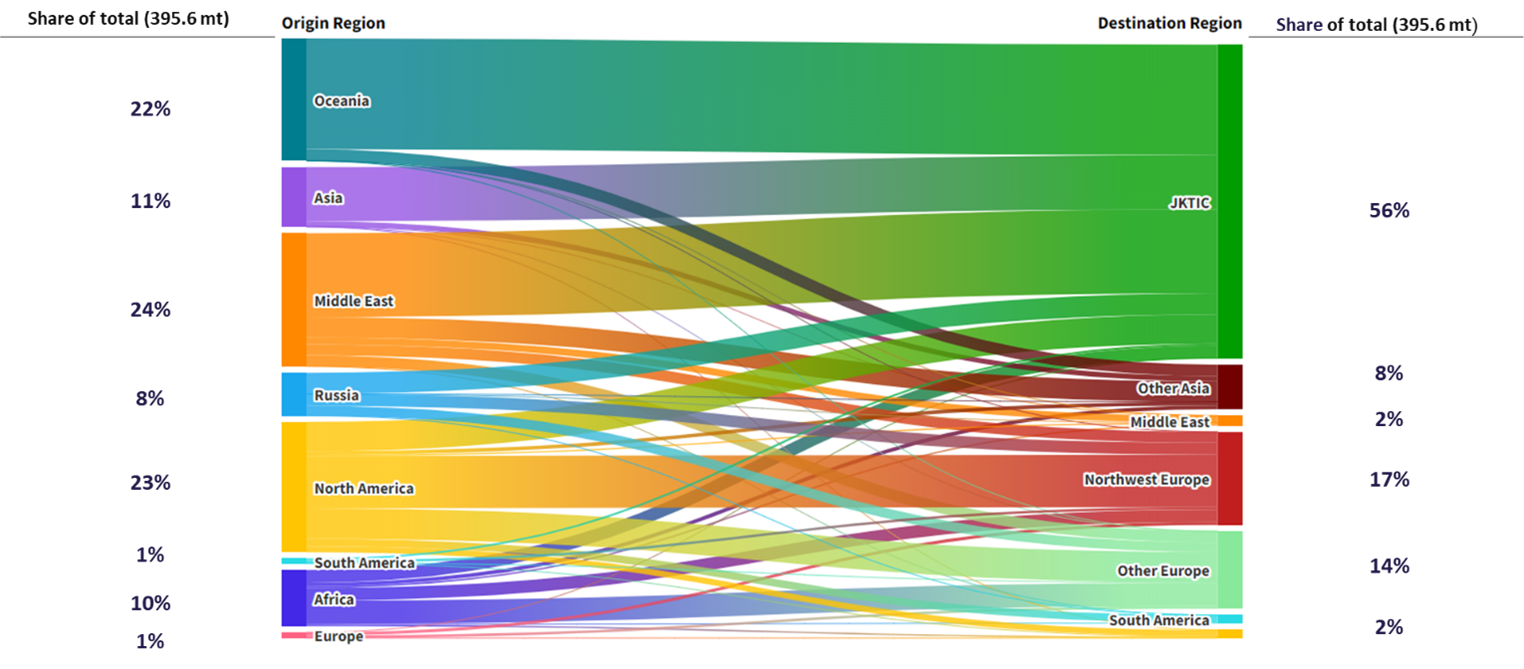

Overall Net LNG Imports saw a modest 1.6% growth to 395.5 mt against a backdrop of limited supply additions

- Overall, LNG imports in 2023 (net of re-loaded exports) grew 1.6% to approximately 395.5 million tonnes (mt), the lowest growth since 2020, when COVID severely impacted demand

- Europe continued to import historically high volumes, with over 65 mt reaching Northwest Europe and 56 mt reaching other European markets (inc. Turkey)

- China and India saw strong returns to demand growth, with imported volumes growing by 14% to 72mt and 10% to 22 mtpa respectively, although total imported volumes remain below 2021 levels for both markets

- On the supply side, the US officially became both the largest global supplier, surpassing Qatar with ~85 mt of exports, and the largest supplier to European markets

- Russian LNG volumes continue to flow to European and Asian markets despite the pressures of sanctions, imposed by Western governments

Net LNG Flows, 2023

Based on preliminary vessel tracking data

Source: Vortexa, Energex analysis

Key Themes to Monitor in 2024

- Limited new supply – 2024 is expected to be the last year of modest growth (approx. 16 mtpa or 3.5%) before a major supply wave begins in 2025. In 2024 we expect Plaquemines Phase 1, Arctic LNG 2 train 1 (despite international sanctions), Tortue FLNG and Congo FLNG to begin exporting volumes

- Development of pre-FID projects –the recently announced pause on approvals of LNG exports to non-FTA by the USA Department of Energy will alter the perception of “next wave” projects in the US. While there is no impact on new volumes coming from those already approved, the role of the US as a major contributor to new supply needed from the early 2030s will be subject to uncertainty and will impact buyer behaviour

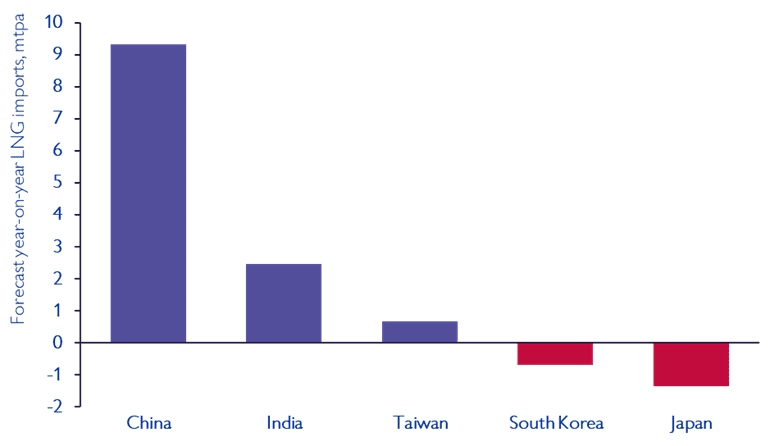

- Recovery in demand due to lower spot prices – Q4 2023 saw strong recovery in demand across China and India as spot prices fell and the JKM/TTF spread widened. How demand in China and other key Asian markets continues to evolve will be key to spot availability of LNG for Europe given limited supply additions

JKTCI YoY demand change outlook, 2024 vs 2023

Source: Vortexa, Energex analysis

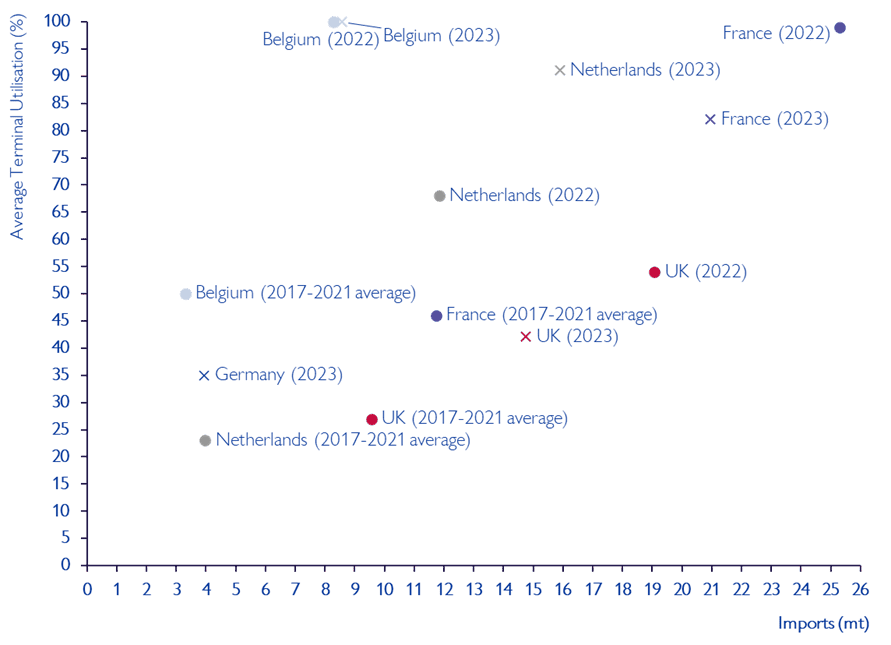

Northwest European regasification terminals continued to see high utilisation in 2023

- Overall, LNG imports into northwest European markets equalled 65 mt in 2023, on a par with 2022 as the continent continues to adapt to gas markets changes following the curtailment of Russian pipeline volumes

- Utilisation levels remain materially higher across NWE versus the five-year average pre 2022, highlighting the intrinsic value of European regasification capacity

NWE country level regas utilisation, 2017-2023

Source: Vortexa, Energex analysis

Key Themes to Monitor in 2024

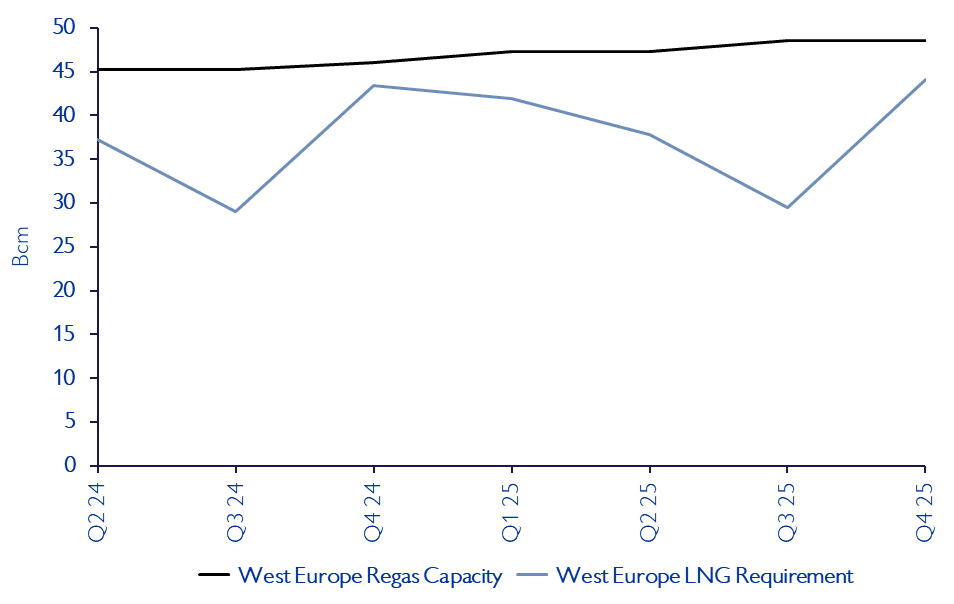

- How terminal utilisation levels in 2024 will evolve – factors influencing terminal utilisation will include storage withdrawals over the remaining winter period (with current levels at 71%, on course to end the winter season above the EU’s target of 50%), what level of demand response we see in Europe as prices continue to fall, and how the ongoing commissioning of new capacity in Germany continues to develop

- An uptick in commercial activity – across both primary and secondary regas contracting and increased M&A activity as market participants look to both capitalise on current pricing dynamics and position for the upcoming new wave of supply entering the market

European LNG requirements versus installed regas capacity, 2024/25

Source: Energex analysis, Bloomberg, Stratas Advisors

Pricing Dynamics

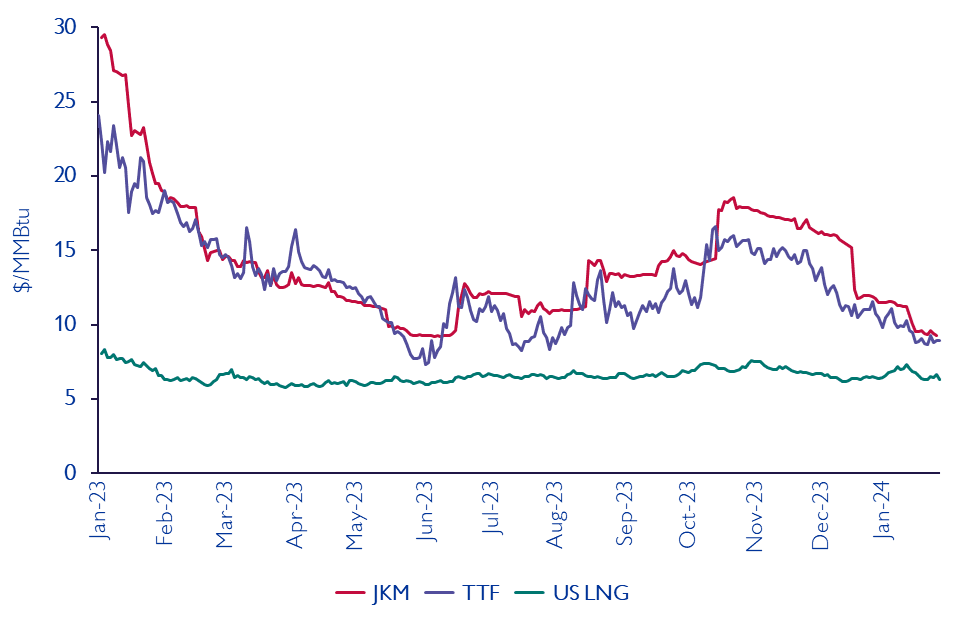

- Outright prices have fallen faster in 2023 than many in the market expected as Europe weathered the storm of lost Russian supplies aided by mild weather conditions, healthy storage levels and the rapid buildout of new LNG terminal infrastructure. Year on year, TTF prices have fallen from over $22/MMBtu to $9/MMBtu, with JKM likewise falling to $9.50/MMBtu from similar levels

- Whilst the numbers have narrowed in January, the spread between JKM and TTF remains consistently positive, providing a strong indicator of demand for cargoes in East Asia

2023 LNG and Gas market pricing dynamics

Source: NYMEX, ICE Endex, ICE Futures Europe

Key Themes for 2024

- TTF / NWE LNG spread evolution – as Germany concludes the commissioning on new FSRU infrastructure bringing more regas capacity to the market

- Competition for volumes between Europe and Asia – and how this will continue to drive JKM and TTF pricing levels. With limited new supply and demand rebounding in Asia, we expect this to be more pronounced in 2024

- Continued arbitrage opportunity for holders of flexible US liquefaction capacity – as Henry Hub prices remains low (between $2.50 and $3/MMBtu) relative to European and Asia benchmarks. However, reports of slowing growth in shale production are expected to apply upwards pressure to Henry Hub prices over 2024.

Much like the past two years, 2024 promises uncertainty, challenges and opportunities in global LNG and gas markets. Energex have been actively supporting new market entrants and established market participants across the gas & LNG value chain – please reach out to Adam Doran or Tom Field to find out more.