The EU Emission Trading Scheme Price Has Evolved – But no one has a Crystal Ball

The EU Emissions Trading System (ETS) has seen prices climbing from under €10/t decade ago to a peak of over €100/t in early 2024 creating a momentum for decarbonization in Europe. Yet since then, the ETS market has shown volatility, with ETS prices fluctuating in the €65–80/t range over the past two years. This trajectory reflects the impact of tightening climate policy – driven by the EU’s Fit for 55 package and the phased reduction of free allowances – but also highlights just how unpredictable the ETS can be.

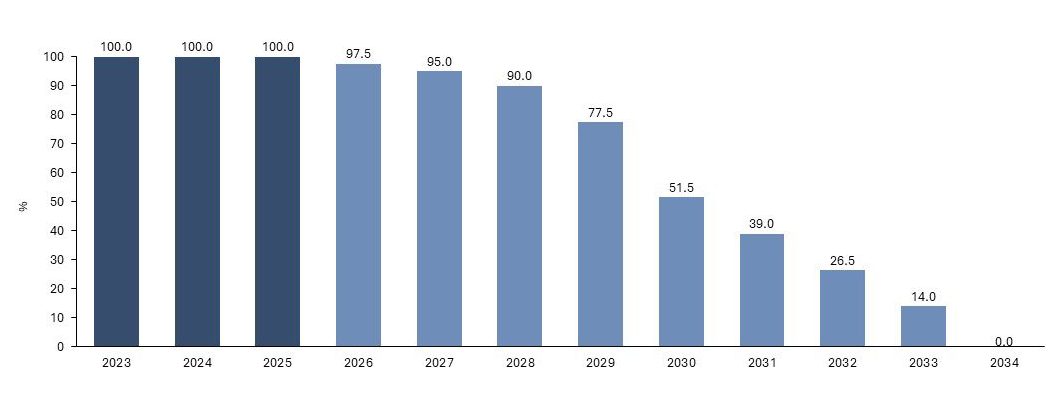

Figure – 1 EU ETS Phase out (% of Free Allowances based on industry benchmarks)

Source: EU

Source: EU

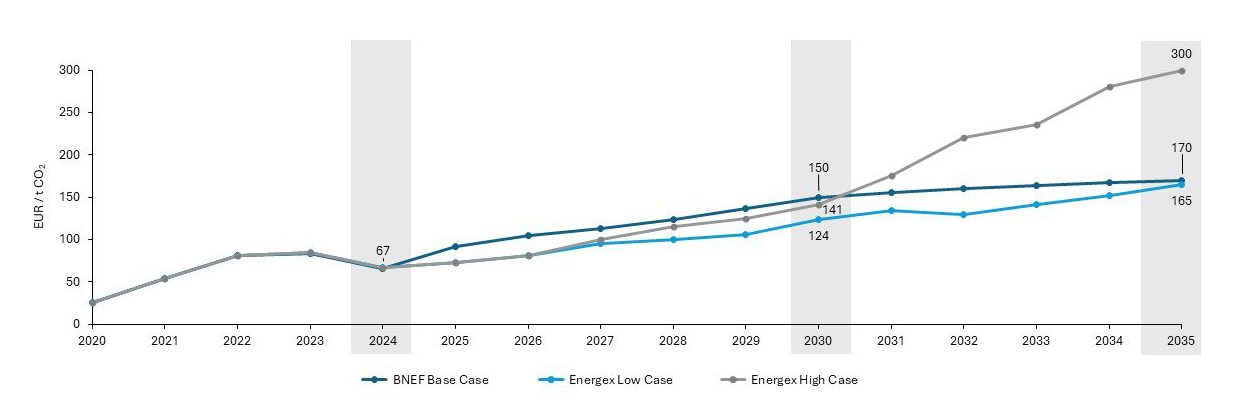

Forecasting where the ETS price will land even a few years from now is a challenge. Analysts such as Morgan Stanley, JP Morgan, and BloombergNEF expect a range: €135–170/t by 2030, and €150–200/t or more by 2035. Energex analysis has a range of €187 to €253 by 2036. ETS Prices are shaped by shifting regulations, energy dynamics, geopolitical events, and market sentiment – all of which can introduce significant volatility.

For project developers and investors, this means carbon price assumptions should be approached with caution. To remain investable and competitive under market scenarios, business models must be robust and resilient across a broad spectrum of future ETS prices, as even a €10-15 fluctuations in the ETS price directly impacts the viability.

Figure – 2 EU-ETS historical prices and forecast

Source: Bloomberg BNEF, Energex Analysis

Understanding the Full Cost Stack

To make the case for a Capture project, it’s critical to look beyond the revenue side and into the full cost stack – especially as most of the costs are fixed at the time of final investment decision (FID).

Here’s a simplified breakdown

- Capture Costs: These vary depending on CO2 concentration, technology, and energy inputs. Operational (OPEX) costs typically range between €40–70 per ton of CO2, with electricity price / utility costs being a key driver. This is in addition to the CAPEX of the plant.

- Transport & Storage: Includes pipelines, terminals, shipping (where relevant), and offshore or onshore injection. Depending on the location and complexity of the chain, costs can range from €30–150 per ton/CO2 (with lower end costs for Onshore CO2 storage and higher end for Offshore CO2 Storage). Transport and storage are typically offered under “send-or-pay” agreements, meaning Emitters must commit to fixed volumes and prices at FID – regardless of future operational performance.

Diversifying Revenue Streams and Making Them Resilient

A resilient capture project structure spreads risk and brings stability across financing, operations, and long-term value.

- EU ETS / Avoided Emissions

- The primary value lies in avoiding the purchase of carbon allowances under the ETS, which can materially reduce compliance costs for emitters.

- While this mechanism supports the project’s business case, it is volatile and difficult to hedge given the uncertainty of future ETS prices.

- As a result, avoided ETS costs alone cannot provide a stable enough revenue base to justify a final investment decision.

- Green Premiums and Offtake Agreements

- Customers may agree to pay higher prices for low-carbon products such as green steel, green cement, or low-carbon fuels, which creates additional revenue for the project.

- Such agreements provide commercial certainty, improve the credit profile of the project, and make business case more viable.

- The effectiveness of this revenue stream depends heavily on the willingness of buyers to pay a premium and on broader acceptance of low-carbon products in the market.

- Carbon Dioxide Removals (CDRs)

- High-value CDR credits can be monetized where a portion of the captured CO2 is biogenic, with waste-to-energy plants typically achieving 30–50% and cement kilns around 5–15% in Europe.

- Operators can actively increase this share by improving their waste-biomass supply chains, deploying biomass drying, or hydrogen boosting into the fuel mix to improve biomass content in the fuel mix.

- These CDR credits can sell for €150–300/t, significantly enhancing project economics, although the market is narrow and depends on the offtake of a few large corporate buyers such as Microsoft.

- Carbon Contracts for Difference (CCfDs)

- CCfDs are government-backed contracts that guarantee a minimum carbon price for the project over a long period of time.

- They provide revenue certainty and act as an effective hedge against fluctuations in ETS prices, which reduces financing risk.

- Access to CCfDs is subject to government policy frameworks and competitive allocation processes, so their availability is not guaranteed for every project and is not available in all countries at this moment.

- Public Funding (EU Innovation Fund, National Grants)

- Public grants are non-dilutive sources of capital that reduce the upfront investment required for capture, transport, and storage infrastructure.

- These funds help close the gap between project costs and revenues, which improves internal rates of return and unlocks private financing.

- They are particularly critical for first-of-a-kind or early commercial projects, though obtaining them requires complex, competitive, and time-consuming application processes.

- Industrial Co-investment and Firm Offtake

- Customers of the emitter can participate directly in the project as equity partners or anchor offtakers, going beyond simply paying a green premium.

- For example, airlines have become investors and committed offtakers in e-SAF projects, while shipping companies are entering into long-term offtake agreements in e-methanol projects. Both approaches provide demand certainty and strengthen the project’s commercial foundation.

- This dual role of co-investment and offtake improves creditworthiness, aligns interests across the value chain, and creates more durable commitments than offtake agreements alone.

Case Study

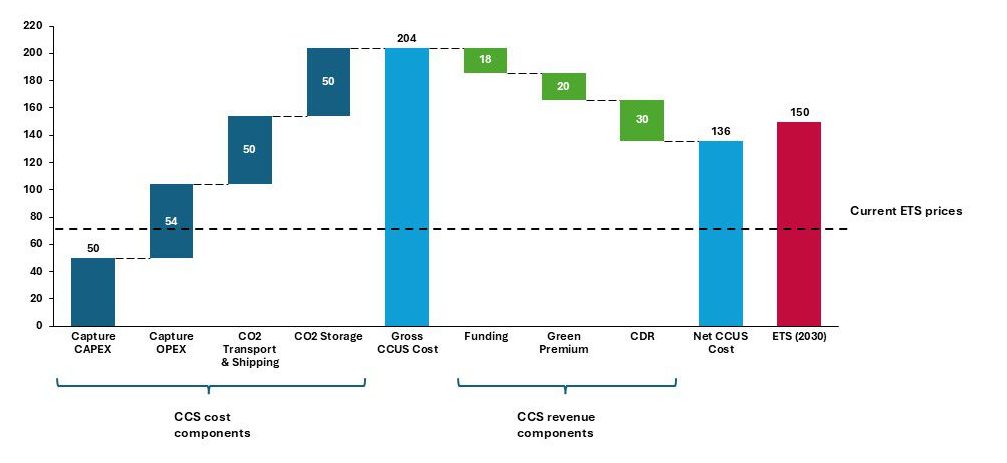

Consider a cement company evaluating a CO2 capture investment at an industrial site in Western Europe. At an ETS price of around €150/ton in 2030, the avoided emissions revenue was not enough to cover capture, transport and storage costs, and the overall economics will not support a final investment decision.

To close the gap, the project may have to integrate:

- Provided they qualify, sale of Carbon Dioxide Removal (CDR) credits at €200/ton for the 15% Biogenic portion of the captured CO2,

- Approximately €125 million in public grant funding (approximately 33% of Capture plant capex) through a combination of EU Innovation Fund or National Funding

- A modest 5% green premium and a firm offtake of the green products.

Figure 3 – CCS Gross and Net Costs against projected ETS price (euro/ton CO2)

Source: Energex Analysis

This combination of revenue streams can transform the project’s economics, shifting it from financially marginal to investable.

Risk Management Is Just as Critical

In addition to revenues, how risks are allocated and mitigated across the value chain is a key factor in project investability – especially for first-of-a-kind CCUS projects. Risks include construction delays, project delays between different parts of the CCUS value chain, regulatory shifts, or offtake underperformance.

Effective risk management follows the principle of treat, take, or transfer:

- Treat through robust design (commercial as well as technical), clear performance guarantees, and milestone-based funding to reduce the probability of failure.

- Take by consciously retaining risks that can be absorbed within the project consortium, for example certain operational risks that are manageable by experienced operators.

- Transfer via mechanisms such as revenue-sharing, risk-pooling, or insurance products. Insurance is emerging as a tool, but is rarely sufficient on its own. Unless a project shows that the other methods are in place, insurers are unlikely to underwrite. New products such as coverage for cross-chain performance or revenue disruptions may help bridge residual gaps, but only if combined with strong upfront structuring.

Developers need to build the capability to identify, assess, and mitigate these risks holistically. This includes not only technical and commercial structuring, but also mechanisms like performance guarantees, milestone-based funding, and risk-sharing agreements. A well de-risked project is often far more attractive to funders than one relying solely on strong revenues.

Final Thought

The EU ETS creates a powerful incentive – but to date it’s not enough on its own. Capture projects must build diversified revenue models, make revenues resilient, seek to control costs, and put in place a clear risk strategy to attract investment and reach FID.