Discussions around the costs of accessing regasification in Europe often focus only on the terminal costs themselves and not on the full stack costs, which includes the cost to enter the grid with regasified LNG.

This is particularly relevant in the UK, which lays claim to some of the highest grid entry costs for LNG users and is considered by many in the industry as a hinderance to the market’s competitiveness as a destination for cargoes. The high network entry prices have multiple impacts:

- Energy security for the UK, especially in the robust domestic demand, rapidly declining domestic production and increased competition for Norwegian pipeline imports

- Potential impact on the tariffs at the three major UK LNG regasification terminals in the UK as original contracts along with exemptions from Ofgem’s Regulated Third Party Access (“rTPA”) expire and capacity is remarketed through open season processes. Potential users consider capacity value through taking a view on full cost stack economics.

A National Gas working group is considering a fundamental overhaul to the network entry charging structure through a modification to the current regime (UNC 0903[1]). If passed, the value of UK regas capacity would be significantly strengthened as we explore below.

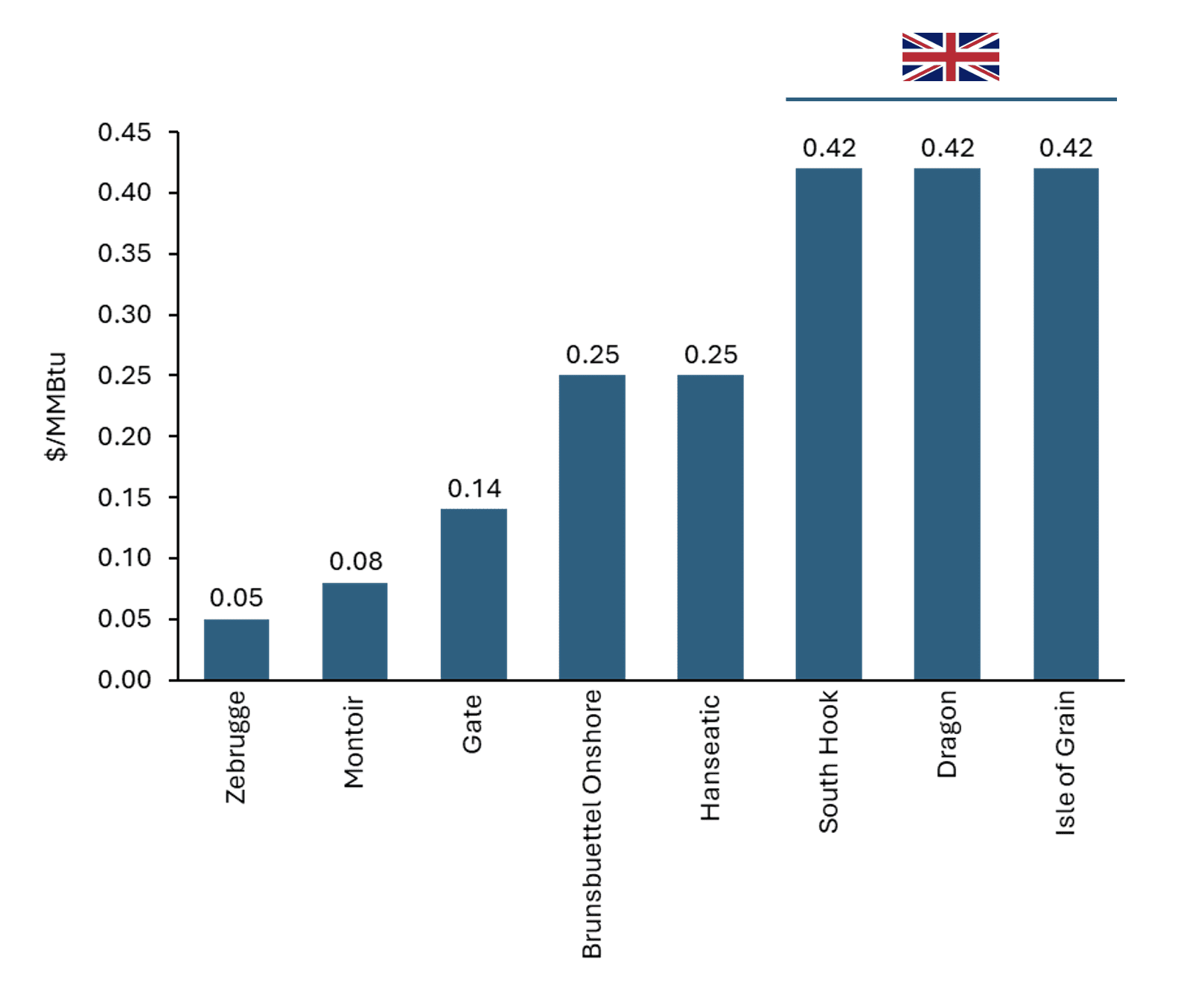

Figure 1 – Comparison of grid entry costs from LNG terminals in Northwest Europe

Source: Published regulated tariffs, Company financials, Energex analysis, UK tariffs re average 2025-2029

Source: Published regulated tariffs, Company financials, Energex analysis, UK tariffs re average 2025-2029

High UK system entry costs for LNG have important impacts on customer appetite, terminal utilisation and pipeline import volumes

On a full stack basis, UK import terminals are more expensive than those in Belgium, Netherlands and France, mainly because of the significantly higher grid entry costs. Among regional terminals, only new German terminals, due to their high development cost, represent a more expensive option at present for LNG players.

This has a direct impact on the relative competitiveness of Norwegian imports and regasified LNG in each market, as it makes the UK a less competitive entry point for LNG in NW Europe; this lowers long-term projected utilisation and exacerbates the impact of declining demand in the 2040s.

The current network charging structure sees UK transmission costs weighted to entry costs

Under National Gas Transmission regulation, the transmission system operator recovers 50% of the ‘Allowed Revenue’ from charges levied at points of delivery to the NTS (‘Entry charges’) with the remaining 50% from charges levied at points of offtake from the NTS (‘Exit charges’).

The comparatively lower aggregate quantity of Entry Capacity procured (compared to Exit Capacity) means that the Entry Capacity charge rate is significantly higher than the equivalent Exit Capacity charge rate.

This has led to two key concerns which have been raised by multiple stakeholders and are now under discussion through a National Gas working group:

- Significant volatility in entry prices as tariffs are calculated on an annual basis

- Concerns that system entry costs at LNG terminals are making UK LNG regasification capacity uncompetitive versus Northwest European alternatives thus threatening UK security of gas supply

The National Gas working group is now considering a fundamental overhaul to the approach of calculating system entry and exit costs

Under UNC 0903, consultations are underway on introducing a single Capacity Reference Price that would be applicable at all Entry Points and all Exit Points. In practice, this means a significant reduction to equivalent entry costs (~50%) and an increase in cost at exit.

On 18th July 2025, a formal consultation with the market was launched which will run until 2nd October 2025. If passed, the changes will bring the UK more into line with other regional markets.

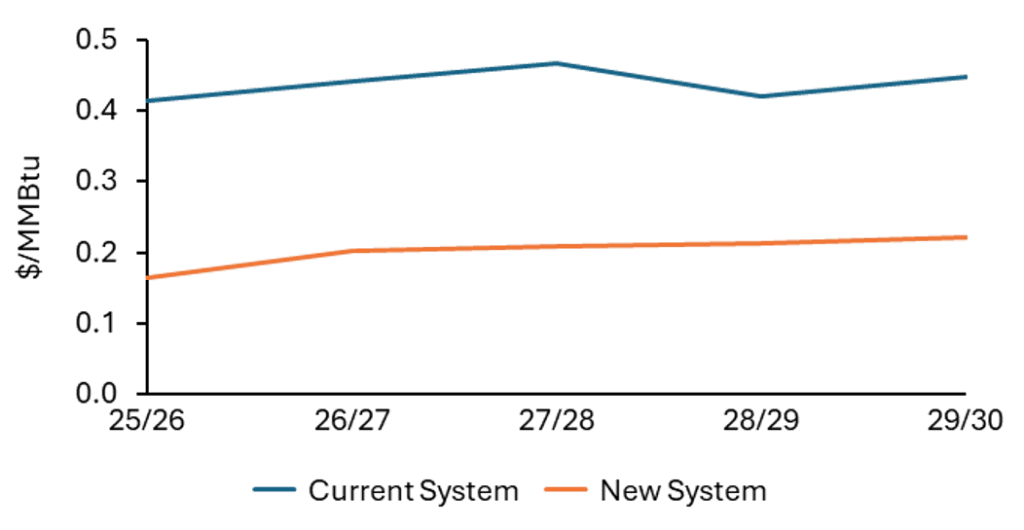

Figure 2 – Current and proposed UK grid entry costs from LNG terminals

Source: Published regulated tariffs, Company financials, Energex analysis; gasgovernance.co.uk

The potential outcome of the UNC 0903 modification is still uncertain and there is no definitive evidence on whether this modification will come into force, but directionally, Energex understands there is good momentum behind it given the Government recognition of the increasing importance LNG imports will play in security of UK supply over the coming decade.

Any changes will need to be published by the end of May ahead of the next subsequent Gas Year meaning the earliest Gas Year this modification could be implemented would be from October 2026.

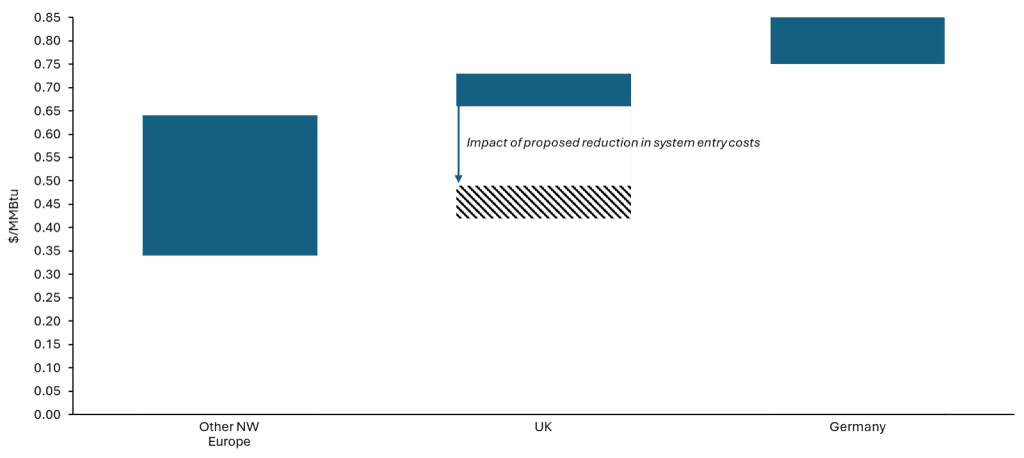

Figure 3 – NWE tariff and system entry costs estimations

Source: Published regulated tariffs, Company financials, Energex analysis

Impact on UK regas tariffs is positive but nuanced

The implementation of UNC 0903 would have a direct impact on the intrinsic value of regas capacity at UK terminals (though the reduction in entry costs would be likely be tempered by a tightening in the NBP/TTF pricing spread), including at Dragon LNG which is currently marketing capacity, and at Isle of Grain which is currently changing ownership from National Grid to a consortium of Energy Capital Partners & Centrica.

Energex is a trusted advisor to the owners, users and developers of regas infrastructure. Please contact Tom Field or Adam Doran if you would like to know more about the work we do.

[1] https://www.gasgovernance.co.uk/0903