The wave of regulatory measures and policy frameworks aimed at decarbonisation is driving the emergence of a diverse array of low-carbon fuel alternatives, from biomethane to hydrogen, each offering its own unique sustainability and value proposition. Commodity traders will need to adapt from markets where supply & demand fundamentals and commodity price dynamics are the norm to fundamentally understand the interplay between environmental mandates, carbon dynamics and the regulatory context.

We explore new trading models and strategies, focusing on the importance of integrating regulations and carbon markets to maximise profit potential and capitalise on emerging opportunities.

Carbon regulations shaping fuel trading markets

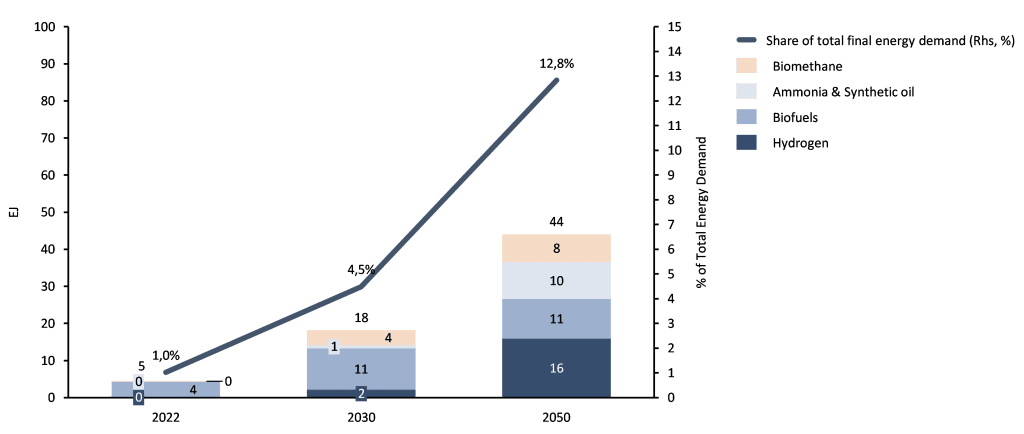

According to the Net Zero Scenario in International Energy Agency’s report, World Energy Outlook 2023, fuels with no or low-carbon intensity like low-carbon hydrogen (green and/or blue), biofuels, sustainable aviation fuel (SAF), methanol, ammonia and biomethane (“low-carbon fuels”) can provide up to 13% of the total final global energy demand by 2050, up from 1% today.

Figure 1 – Low-carbon fuels in total final energy demand

Source: IEA, World Energy Outlook 2023

At the heart of this transformation lies the common thread binding these new products: their origin in regulation and policy. For traders, understanding the intricate interplay between environmental mandates, market dynamics, and technological advancements will be essential as well as the agility to mix asset ownership and short- and long- term contracts.

Unlike traditional commodities where supply and demand dynamics are the foundation, the economic value of low-carbon fuels is closely linked to their environmental impact and regulatory context and carbon dynamics—the complex web of carbon emissions, offsets, and mitigation strategies that will underpin the price of low-carbon fuels.

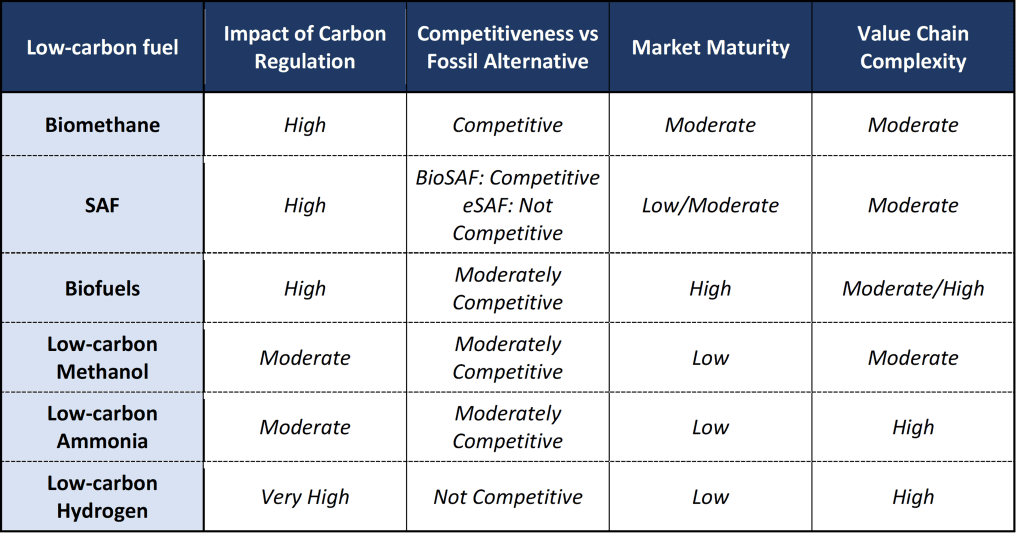

Varied low-carbon fuels linked by common carbon regulations

Each low-carbon fuel offers distinct challenges and opportunities:

- Biomethane: Derived from organic waste or biomass, biomethane exemplifies this convergence of environmental imperatives and market opportunities as it has emerged as a viable alternative for both power generation and transportation. However, its commercial viability depends on very specific value chain factors, including feedstock availability, technological scalability, and regulatory support for renewable natural gas programs.

- SAF: As the aviation industry seeks to mitigate its carbon footprint, SAF has garnered attention. Made from renewable feedstocks, bio-SAF from hydroprocessed esters and fatty acids (HEFA) or municipal waste and eSAF, from synthetic fuel derived from renewable energy, offer a pathway to reducing emissions from air travel and offer arbitrage opportunities where price differentials exist. Yet, the SAF market faces challenges ranging from cost competitiveness of eSAF with conventional jet fuel to scaling up production capacity.

- Biofuels: Encompassing ethanol and biodiesel, have long been heralded as a bridge to a low-carbon future despite issues over land use and food crop competition. Nevertheless, advancements in feedstock diversification and production efficiency continue to bolster the market maturity and offer traders opportunities for hedging and speculative trades.

- Methanol: Increasingly being produced from renewable sources, methanol’s potential as a clean-burning fuel for transportation or as a feedstock for chemical synthesis underscores the growing importance of carbon-neutral pathways in the energy transition.

- Ammonia: Primarily used in fertilisers, is also gaining traction as a low-carbon energy carrier. Produced through electrolysis using renewable electricity, low-carbon ammonia holds potential as a fuel for maritime shipping and a means of storing and transporting renewable energy. However, significant infrastructure investments and technological advancements are needed to realize its full potential in the global energy mix as well as managing safety concerns.

- Hydrogen: A versatile fuel with myriad applications across industries. Whether as a feedstock for industrial processes, a fuel for transportation, or a means of energy storage, hydrogen is poised to play a pivotal role in the medium-long term to decarbonising sectors that are challenging to electrify. Yet, the widespread adoption of hydrogen hinges on overcoming hurdles related to production costs, infrastructure development, and regulatory support.

Figure 2 – Summary of low-carbon fuels

Please note that the above is a high-level summary and might potentially not reflect different conclusions within the same low-carbon fuel when assessing in further detail, e.g. BioSAF vs eSAF, hydrogen competitiveness subject to different end-user demand, value chain complexity will differ across the value chain, etc.

Trading models and strategies to succeed in low-carbon fuel trading

Success in low-carbon fuels markets will demand adjusting and/or adopting new trading models and strategies as commodity traders master evolving regulatory and policy frameworks to accurately assess the value proposition of each low-carbon fuel within rapidly changing supply and demand dynamics. We include below four model examples that can be tailored for new low-carbon fuel trading markets:

- Integrated Value Chain Model: Suitable for markets like biofuels with high maturity and high value chain complexity, trading companies may opt for partial vertical integration, controlling multiple stages of the value chain, from production to distribution. Companies may invest in infrastructure and technology to optimise production processes and enhance efficiency and capture any regulatory optionality between geographical markets.

- Partnership-driven Model: For nascent markets with high value chain complexity scenarios, strategic partnerships with technology providers, research institutions, and regulatory bodies can mitigate risks and accelerate market development. Companies may focus on niche segments or emerging markets where their expertise and resources can create a competitive advantage. Examples include low-carbon hydrogen and low-carbon ammonia, where innovative solutions and collaboration can enhance market intelligence and early-stage market development as well as manage any potential first mover risk in an immature market.

- Compliance-driven Model: In markets heavily influenced by carbon regulation, like hydrogen, trading companies should prioritise compliance with environmental mandates and emissions targets. This may involve investing in carbon capture projects, implementing emission reduction strategies, or trading carbon credits to meet regulatory requirements. Companies may also seek opportunities in carbon trading markets or develop sustainable finance products to align with regulatory objectives. This model also allows for speculative positions in carbon credits and derivatives.

- Innovation-led Model: Where carbon regulation plays a moderate role, such as in low-carbon methanol and ammonia markets, trading companies can focus on innovation and differentiation. This may involve investing in R&D to improve fuel efficiency, reduce carbon intensity, or develop new product variants. Companies may also explore partnerships with technology start ups or invest in pilot projects to test new solutions. Traders can leverage differentiation to create arbitrage opportunities between innovative products and conventional fuels.

In conclusion, commodity traders can capitalise on low-carbon fuel trading opportunities by adopting models and strategies that consider the interplay between carbon regulation, pricing competitiveness, market maturity and value chain complexity, while effectively managing environmental and regulatory risks and contributing to the broader goal of sustainability and climate resilience.

Written by Rui Almeida, Partner: rfalmeida@energex.partners