Our Gas & LNG team reflect on the some of the key themes in LNG and Gas during 2025 and what to look out for in 2026 including market reactions to the first post-2022 year of meaningful supply additions, the outlook for European LNG imports and West-to-East flows, and how LNG portfolio holders manage length through downstream positions and regas access.

Please get in touch with Tom Field or Adam Doran if you’d like a more in-depth conversation.

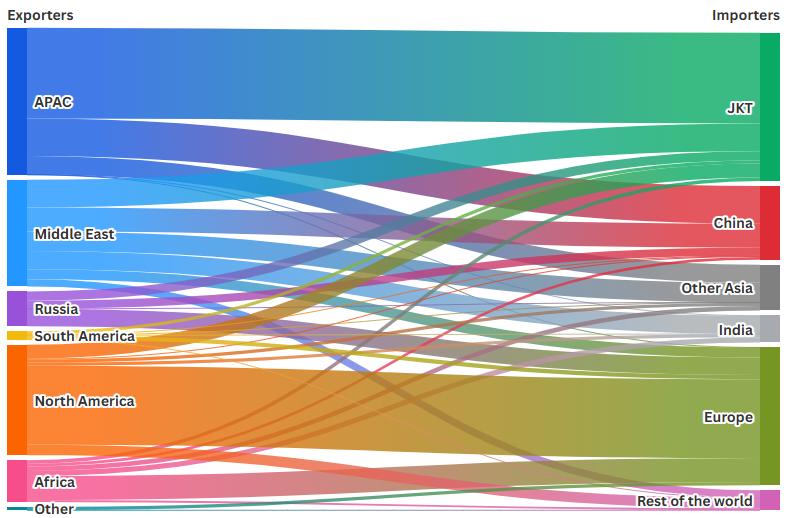

LNG supply reached 435 mt in 2025 – higher European imports required a reduction in Chinese demand, preventing a material price decline

LNG trade in 2025Based on vessel tracking data

|

|

Source: Vortexa, Energex |

|

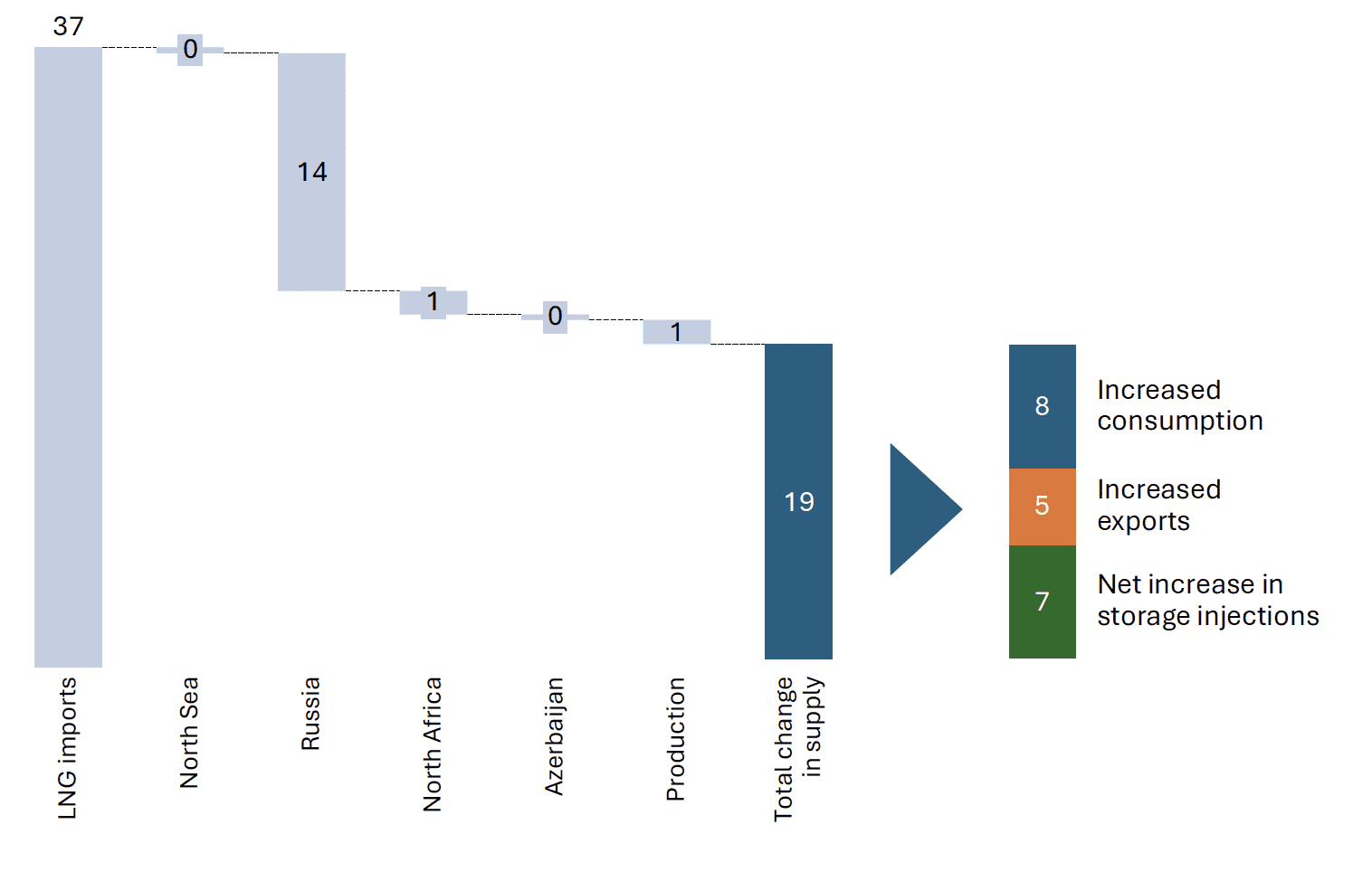

Higher European LNG imports were crucial in refilling depleted storage levels, replacing Russian supply lost at the start of 2025 and meeting demand in the EU and Ukraine

Change in European gas balanceDifference in supply and demand between 2025 and 2024, Bcm

|

| Source: ENTSOG Transparency Platform, AGSI, Energex |

|

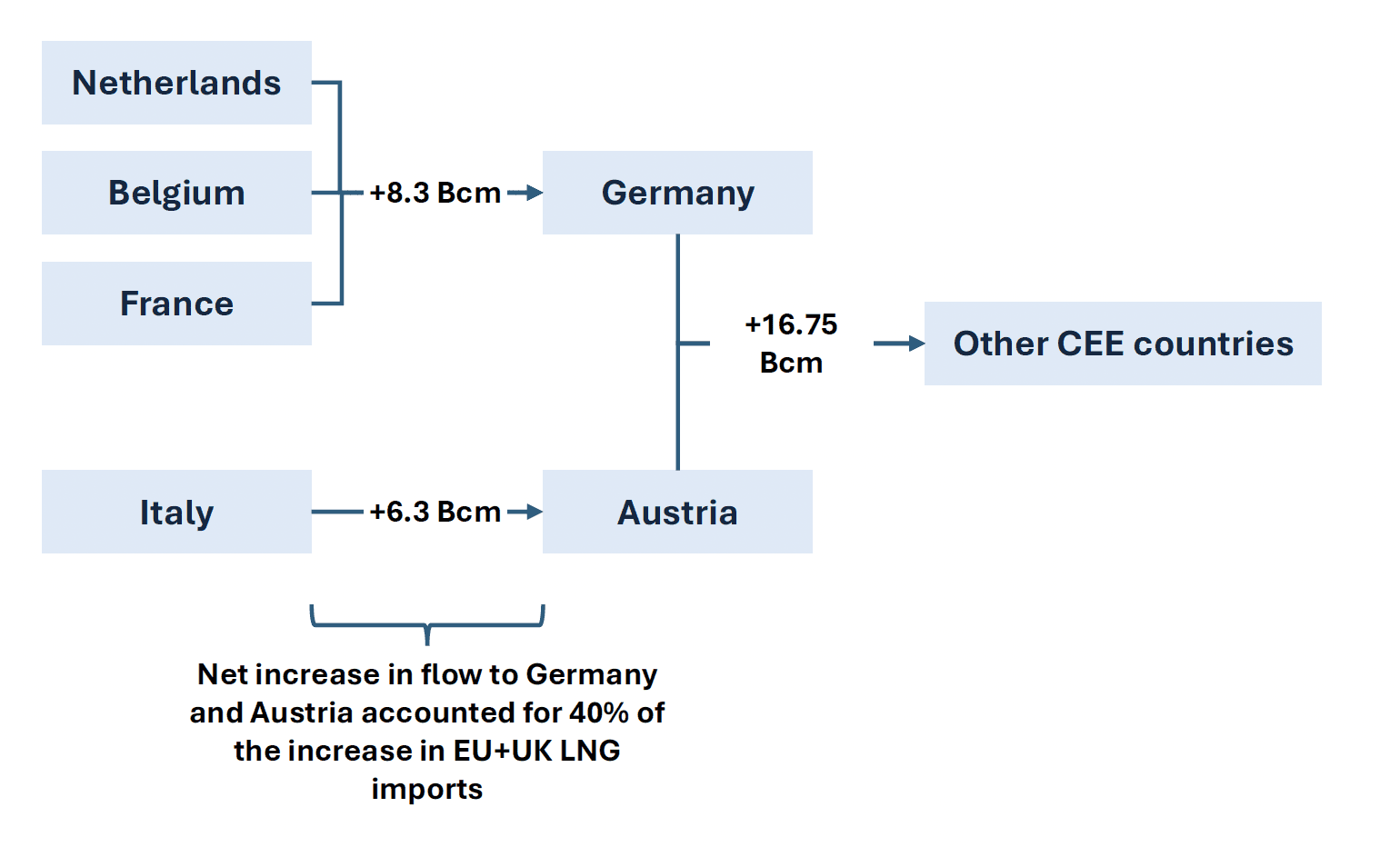

Higher LNG imports in Western Europe and Italy played the most significant role in enabling stronger Eastwards flows

Increase in Eastwards gas flow from key LNG importing marketNet change in gas flows between countries between 2025 and 2024, Bcm

|

| Source: ENTSOG Transparency Platform, AGSI, Energex |

|

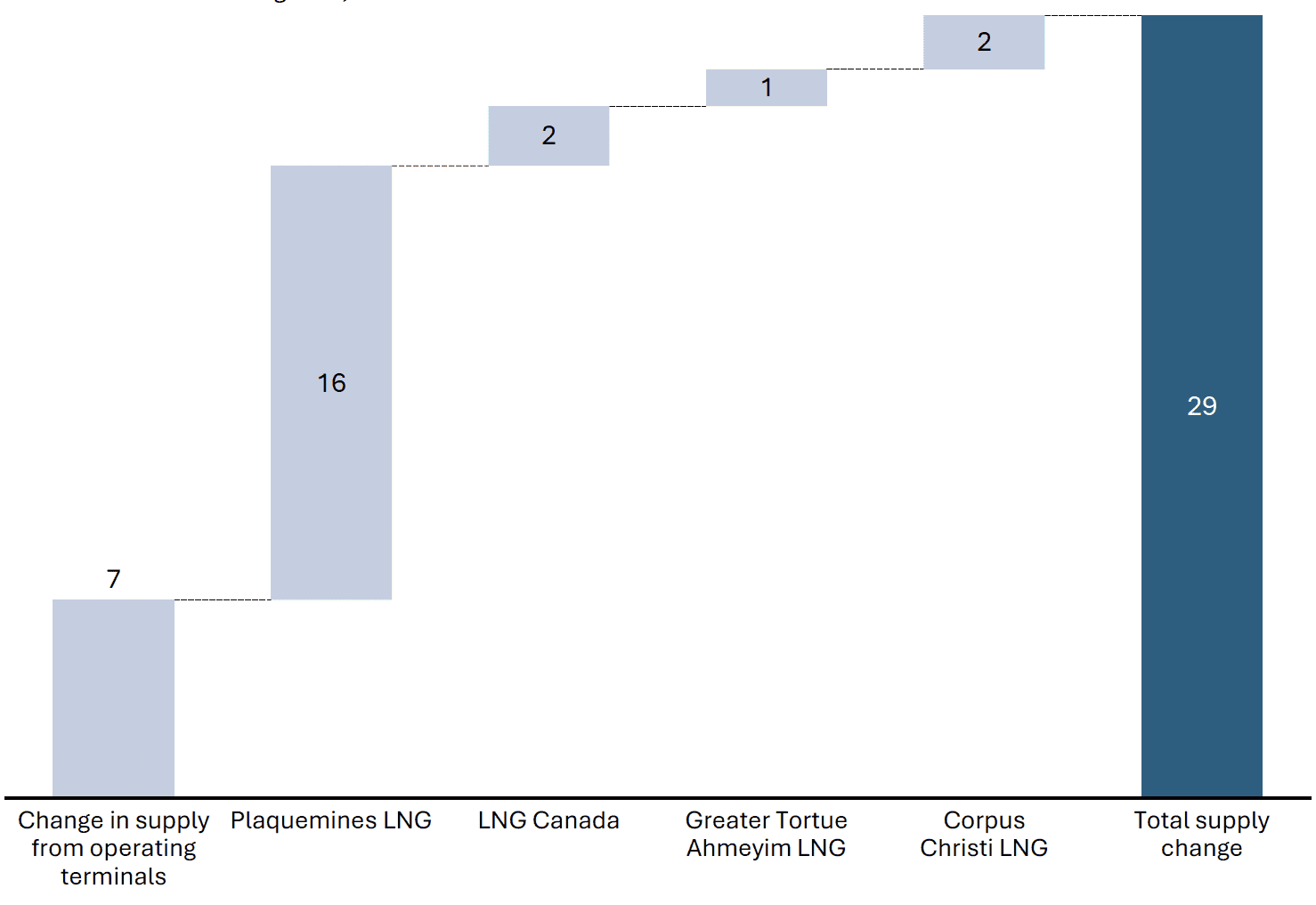

Global LNG supply increased by 29 mtpa, almost entirely due to the ramp up of new North American export projects

2025 increase in LNG supplyBased on vessel tracking data, mt LNG

|

| Source: Vortexa, Energex |

|

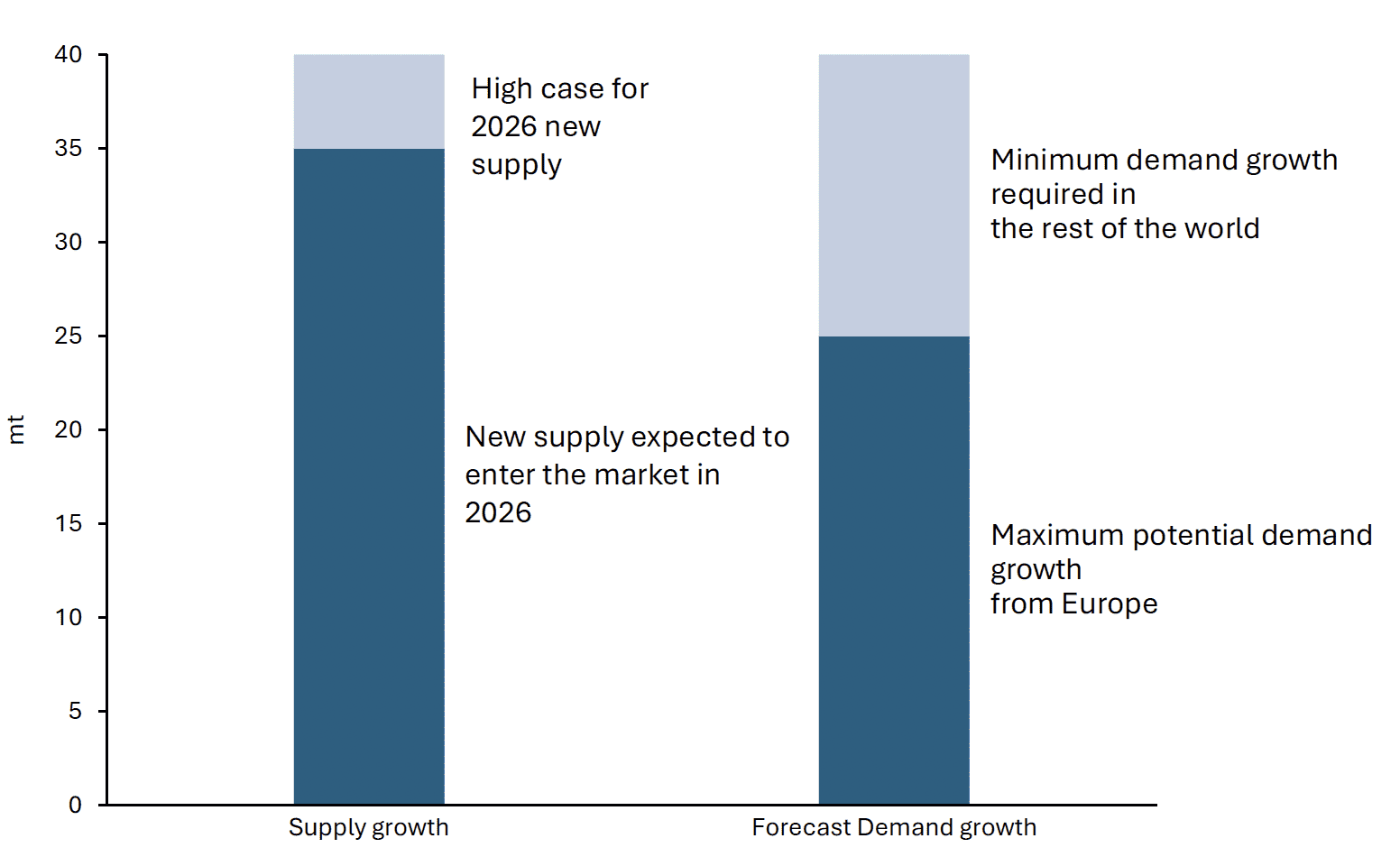

2026 will mark the first year since 2022 in which supply additions may enable prices to remain at sufficiently low levels to stimulate a return to growth by Asian markets

2026 LNG market balanceEstimated based on publicly announced timelines for new projects

|

| Source: Vortexa |

|

Strategies and commercial models will need to adapt to navigate the largest phase of market growth in the history of the LNG industry

|

► |

|

Large volumes of new supply have now started to enter the LNG market, which coupled with stagnating demand growth in Asian markets is likely to have a major impact on market dynamics |

|

► |

|

Multiple new and growing players have built LNG portfolios by acquiring significant supply length in recent years; securing a diverse portfolio of downstream access points will grow in importance to balance and optimise portfolios |

|

► |

|

Access to regasification capacity will be highly valuable; though limited long-term primary capacity is available in Northwest Europe we expect players will seek out capacity with longer-dated commencement to provide balance to growing long positions in portfolios |

|

► |

|

The development of new supply will become more challenging, with stronger competition between pre-FID projects and successful projects likely to require their sponsors taking more market risk |

|

► |

|

Building a deep understanding of and mitigating geopolitical risks is an increasingly key element of successful strategies for LNG market participants in a more volatile and unpredictable world |

|

► |

|

As prices in the spot market and in long-term contracts begin to diverge, margins are expected be squeezed for a period, putting pressure companies to ensure fit for purpose commercial operating models (including the contracts that underpin them) are in place to ensure portfolio optimisation and mitigate value leakage |

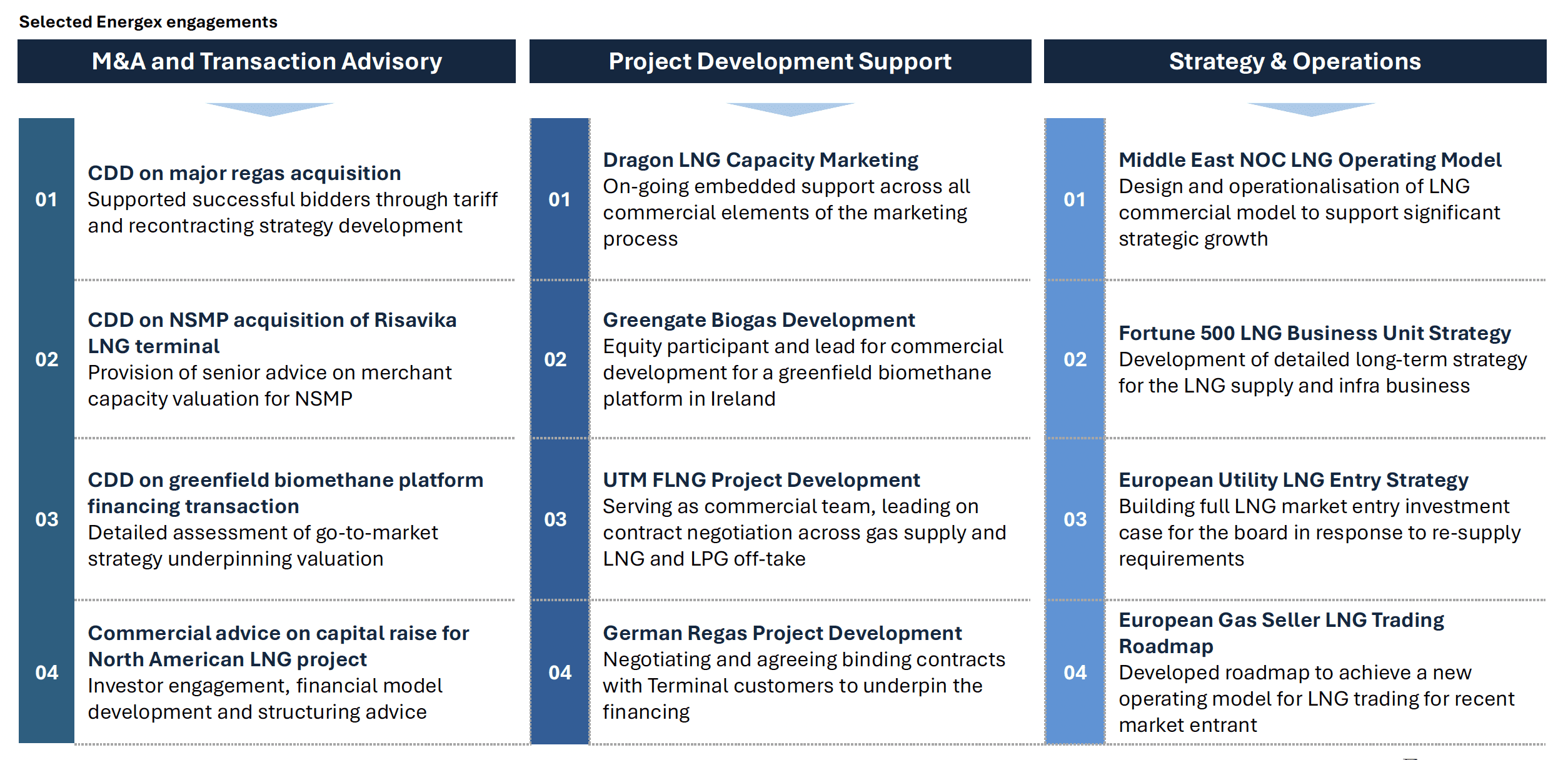

Energex connects practical experience, advisory capability and market understanding to bring clients genuinely differentiated support across the gas and LNG value chain

Energex is a leading advisory business for players and investors in gas & LNG…

Practical ExperienceDeep practitioner experience from leading organisations in supply, trading, M&A and contracting sit at the heart of our team – we are blooded by experience, not just steeped in theory |

|

Hands-on CapabilityEnergex has a track record as an advisor capable of embedding into client teams to drive key initiatives forward – operating model design, LNG offtake, capacity marketing and project development |

|

Market UnderstandingCollectively we bring decades of experience in assessing gas & LNG markets underpinned by global flow and pricing models – we provide flexible analysis to enable scenario thinking |

…our sector focussed team combines practitioner expertise from top-tier organisations with sector specific consulting experience…

Energex is known for our hands-on work for clients on significant strategic initiatives and major transactions across the gas, LNG and biogas value chains