Overview

European industry is entering a period of high compliance costs as the EU Emissions Trading System (EU ETS) tightens, free allowances are phased out and decarbonisation continues to lag.

Launched in 2005, the ETS sits at the centre of the bloc’s climate policy and has grown to become the world’s largest carbon market. Operating on a “cap‑and‑trade” basis, it limits the amount of CO₂ that covered sectors may emit, effectively imposing a cost on emissions that exceed these allowances.

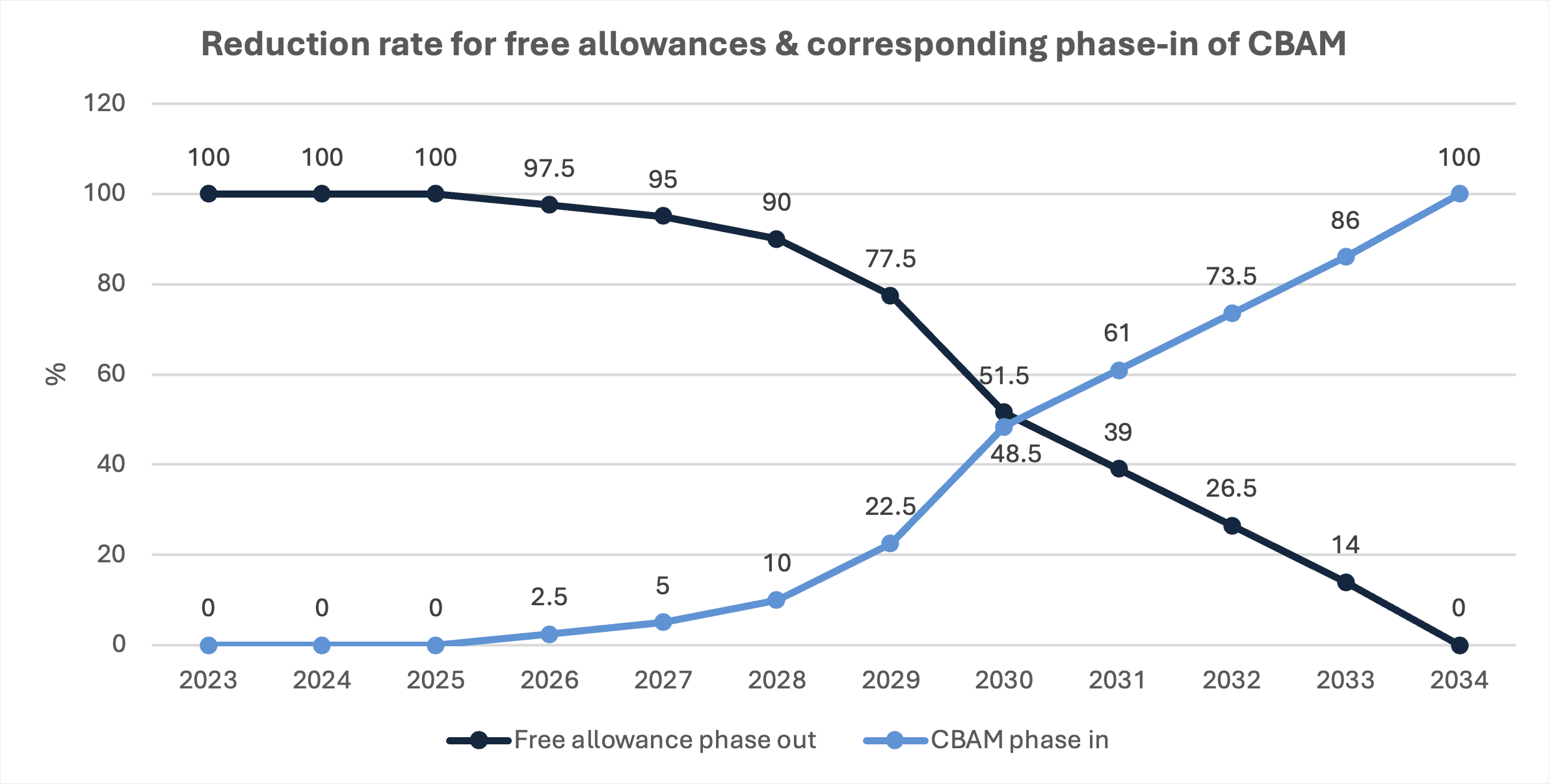

Industrial emitters have long benefited from generous free allowances, but these are set to be phased out over the coming decade. As a result, the market will be increasingly shaped by tightening fundamentals on both sides: supply will be constrained as free allowances are reduced, while demand will depend on how quickly sectors can cut emissions.

In recent months, the ETS has come under increasing political strain, with high energy prices, rising carbon costs and industrial competitiveness emerging as central themes in the debate. Italy’s energy minister has called for an immediate suspension of the ETS, citing the burden of carbon and energy costs, while a group of EU countries (including Denmark, Finland, Portugal, Spain and Sweden) have warned against weakening the system.1

Against this backdrop, EU leaders at the Brussels summit in March dismissed calls to suspend the ETS and instead backed a dual‑track intervention plan, including a €30bn investment booster, industry-friendly benchmarks for free allocations, and adjustments to the Market Stability Reserve to curb volatility.2 Yet major questions remain, particularly around the pace of supply adjustments and the extent of intervention to stabilise prices. A comprehensive ETS review, expected by July 2026, will therefore be central to medium-term market expectations.

European industry is set to face rising compliance costs as free allowances are reduced and decarbonisation lags

Historically, heavy industry has benefited from generous free allowances, but this protection is set to diminish as allowances are phased out and the market tightens. In the near term, most abatement will continue to come from the power sector, supported by the expansion of renewables. However, as lower‑cost decarbonisation options are exhausted, pressure will increasingly shift towards heavy industry, where emissions are harder and far more expensive to eliminate.

While green hydrogen and carbon capture offer abatement pathways, high capital intensity and challenging economics have kept investment well below required levels. Many projects are in planning stages or have been affected by a wave of cancellations, as we are witnessing with green hydrogen projects across Europe. At the same time, current carbon prices remain below the levels needed to trigger major industrial decarbonisation, since marginal abatement costs in industry are materially higher than in the power sector.

With progress still lagging, industry is entering the next phase of the ETS underprepared, leaving emitters exposed to much higher prices and sharply rising compliance costs.

Oil refining stands out as one of the sectors most exposed to rising carbon prices

As the market tightens, refining is the sector most exposed to rising carbon prices, since it is not covered by carbon‑leakage3 protection mechanisms such as the CBAM. With limited abatement solutions in place, many installations will be left with little choice but to absorb the full carbon price. This is expected to drive costs sharply higher and leave parts of the sector uneconomic relative to international competition, increasing the risk of closures.

Exxon has warned that all UK refineries may close due to carbon costs, adding that its Fawley refinery, the UK’s largest, was expected to spend about £70–80mn on CO₂ costs in 2025, rising to roughly £150mn over the next 4–5 years.4 Similarly, the EU refining sector could face compliance costs running into the billions across the coming years, as progress in reducing emissions remains limited.

With security of supply and energy affordability high on the policy agenda, industry will require much stronger policy support, greater funding and substantially more infrastructure investment than is available today.

Deep Dive:

Decarbonisation has been driven by the power sector so far; pressure now shifts to industry as easier gains fade

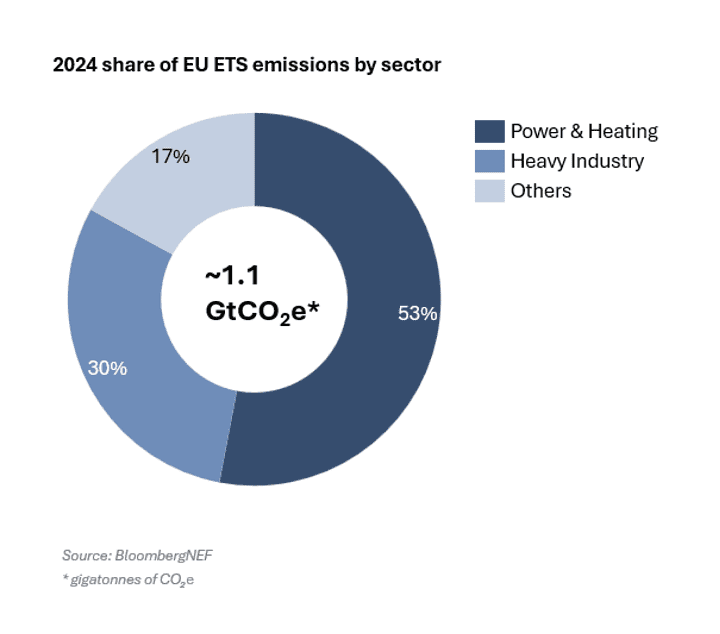

The power sector accounts for more than half of emissions covered by the ETS and has also been the main driver of emissions reductions, supported by rapid renewables growth. Looking ahead, electricity demand is expected to rise materially, driven by EV uptake, industrial electrification and the expansion of data centres. Emissions could fall further if renewable deployment accelerates sufficiently, but this will also hinge on solving challenges such as availability of battery storage and intermittency.

Outside power, industrial sectors (including steel, refining, cement and chemicals) are the largest contributors to emissions and account for a significant share of EUA demand.5 As emissions in the power sector continue to fall, many of its lower-cost abatement options will gradually be exhausted. Attention will then turn to industry, where emissions are technically harder and more expensive to eliminate.

Industrial decarbonisation remains nowhere near the scale required

Heavy industry does not meaningfully start to decarbonise at today’s carbon prices and needs much higher prices to make low‑emissions technologies viable. For instance, a CO₂ price above 147 EUR/tCO₂ is needed to make the hydrogen-based DRI-EAF route competitive versus fossil intensive routes in steel.6 Similarly, many sectors need carbon prices between 100–200 EUR/tCO₂ for low emissions options to become economic.

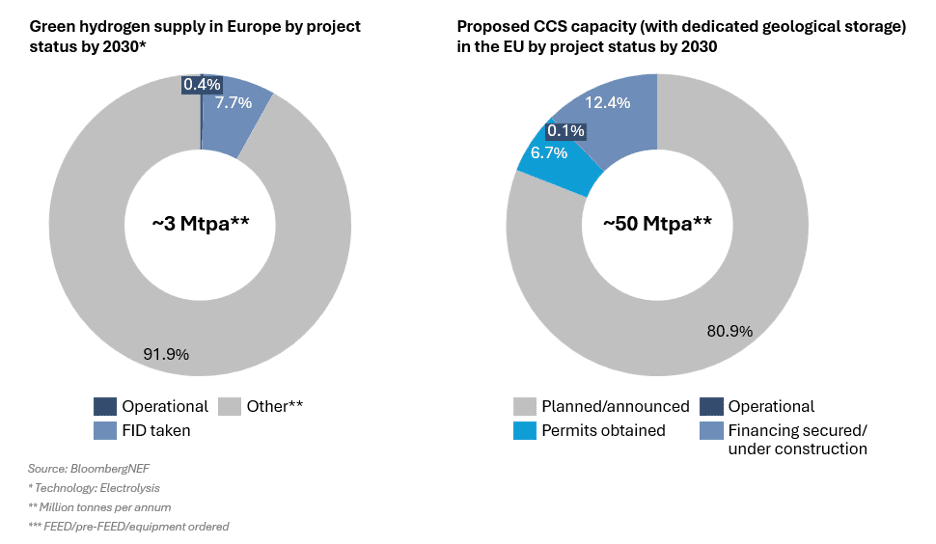

Green hydrogen and CCS (Carbon Capture and Storage) are among the most common pathways for deep industrial decarbonisation, but deployment is still far below what is required. According to Bloomberg data, only 0.1% of announced CCS projects is expected to be operational by 2030. Meanwhile, several high‑profile hydrogen projects have been delayed or cancelled as regulation lags and project economics remain challenging.

The result is that industrial decarbonisation is falling far behind the pace at which free allowances are being withdrawn, creating an urgent need to accelerate the deployment of low‑carbon technologies.

CBAM may not serve as a perfect tool for protecting competitiveness

Parallel to rising EU ETS prices, carbon markets will increasingly be shaped by the Carbon Border Adjustment Mechanism (CBAM). Introduced as the EU’s primary tool to prevent “carbon leakage”3, CBAM places a cost on emissions embedded in carbon‑intensive imports entering the EU. Its objective is to level the playing field by ensuring that imported goods face a carbon price comparable to that borne by domestic producers under the EU ETS. Sectors currently covered include cement, iron and steel, aluminium, fertilisers, hydrogen, and electricity.

Sectors like oil refining fall outside the scope of CBAM and are among the most exposed to rising carbon prices. Bloomberg notes that European refiners could face compliance costs running into the billions by the end of the decade. This pressure comes against a backdrop of continued capacity loss, despite supportive margins in 2025. The EU has lost almost 500 kb/d of refining capacity, and the UK has seen two of its six refineries close. European refiners warn that the sector risks becoming uneconomic in global markets without stronger import protections, posing what they see as an existential threat to its future.7

Even for sectors covered by CBAM, the mechanism has been hampered by persistent implementation challenges. Importers and domestic producers have had to navigate evolving rules, pending technical guidance and uncertainty over how embedded emissions are calculated and verified, making compliance costs difficult to anticipate. Recent policy moves have added further uncertainty. For instance, the Commission’s proposal to suspend import tariffs on ammonia and urea, followed shortly by an “emergency‑brake” mechanism (that would allow for a temporary suspension of CBAM for specific goods), has added another layer of complexity for importers.9

These shifting policy signals risk weakening the intended alignment between the EU ETS and CBAM. For sectors set to lose free allocation, CBAM may therefore prove an imperfect tool for preserving competitiveness.

Conclusion

We draw on BNEF’s sector‑specific carbon pricing model (EUCPM 2.1) to inform our view of the decarbonisation trajectory across the industrial stack and its implications for carbon prices. Assuming the current pace of decarbonisation and planned phase-out of free allowances continue without changes, Energex expects carbon prices to reach €200/tCO₂ by 2035.

As prices cross a certain threshold, two outcomes are likely to emerge in the market:

- investment in emissions reduction where economically viable

- facility closures where it is not

However, the price trajectory is becoming increasingly uncertain as political pressure builds amid high energy prices and the ongoing war. As a result, the policy path may shift in response to changing conditions, making the upcoming ETS review crucial for shaping medium‑term expectations.

Against this backdrop, industrial decarbonisation will still require a strong and predictable carbon price signal, supported by adequate policy and investment measures to improve economic viability and move projects towards final investment decisions.

Understanding carbon market developments has become crucial for asset owners and project developers across multiple sectors. Energex is well positioned to offer expert support through our senior practitioners, each with more than 20 years of experience across carbon markets, CCS value chains, low‑carbon molecules, and refining. Our analysis is supported by a robust methodology that captures key dynamics shaping the EU ETS market, and can be tailored to meet specific client requirements. We also bring extensive low‑carbon expertise and a strong track record in securing public funding, including successful applications to the EU Innovation Fund.

Please contact us at info@energex.partners to discuss the contents of this article, carbon markets or public funding in more detail.

References

1 Quantum Commodity Intelligence: Group of EU nations warn against ETS weakening ahead of summit

2 Quantum Commodity Intelligence: EU leaders agree to “preserve” ETS, back dual-track intervention

3 According to the European Commission, “‘carbon leakage’ refers to the transfer of CO₂ emissions from one country to another when, due to strict climate policies, companies relocate their production to countries with weaker emission constraints.”

4 Bloomberg: All UK Oil Refineries May Close Due to Carbon Costs, Exxon Says

5 EUA: EU Allowance

6 DRI-EAF: Direct Reduced Iron-Electric Arc Furnace; JRC: Mapping the transition of the EU steel industry to carbon neutrality

7 S&P Global: European refiners plead for CBAM protections

8 S&P Global: EU publishes CBAM emergency brake guidance after fertilizer backlash